| Indian nationals can open a Bangkok Bank savings account in Thailand, but success depends heavily on visa type. For those researching a Bangkok Bank account Indian nationals guide, LTR Visa holders (with BOI endorsement letter) and Non-Immigrant visa holders (with work permit) have the clearest pathway. Tourist visa holders are typically rejected. Required documents include: Indian passport, visa document, rental contract or proof of Thai address, and passport-size photograph. The account opening process takes 30 to 60 minutes at the branch. Minimum opening deposit is typically THB 500 to THB 1,000. Bangkok Bank is Thailand’s largest bank and the most recommended for foreign nationals due to its international network and foreigner-friendly branch staff. For receiving international income (USD, EUR), Wise is a significantly cheaper alternative to SWIFT transfers into a Bangkok Bank account. |

| QUICK ANSWER: Can Indian nationals open a Bangkok Bank account in Thailand? Yes, Indian nationals can open a Bangkok Bank account in Thailand, with the following conditions: LTR Visa holders: YES — easiest pathway; BOI endorsement letter accepted Non-Immigrant B (work visa) holders with work permit: YES — standard process Non-Immigrant O (retirement/family) holders: YES — with supporting documents Tourist visa holders: DIFFICULT — most branches reject; rare exceptions exist Visa-exempt entry holders: Very difficult — not recommended to attempt Documents needed: Indian passport, valid visa, proof of Thai address (rental contract), 1 passport photo, initial deposit of THB 500–1,000. |

| DISCLAIMER Bangkok Bank requirements for foreign nationals, including Indian passport holders, can change without notice. Requirements vary by branch and are subject to manager discretion. Always verify current requirements directly with Bangkok Bank (bangkokbank.com) or by calling the specific branch before visiting. This is not financial or legal advice. |

Introduction

Opening a Bangkok Bank account is one of the most commonly asked banking questions among Indian nationals living in or relocating to Thailand. And it is also one of the most frequently answered incorrectly — usually by guides that list documents without addressing the most important variable: your visa type.

The reality is that Bangkok Bank’s ability to serve Indian nationals depends almost entirely on what type of visa you hold at the time of application. An Indian professional on an LTR Visa with a BOI endorsement letter will have a straightforward 45-minute account opening. The same person on a tourist visa will likely be turned away, regardless of how complete their documents are.

This guide covers the full picture: which visa types qualify, the exact document list, which branches to visit, the step-by-step process, fees, SWIFT transfer guidance for sending money to India, the FEMA implications of holding a Thai account, and the Wise alternative that many Indian remote workers prefer for international income.

The Critical First Question: Which Visa Do You Have?

Bangkok Bank, like all Thai commercial banks, uses your visa type as the primary eligibility filter for foreign national accounts. Here is the current landscape for Indian passport holders:

| Visa Type | Account Opening Possibility | Additional Notes |

| Thailand LTR Visa (WFT or other categories) | ✅ Easiest pathway | BOI endorsement letter is strong proof of legal long-stay status. Most branches familiar with LTR Visa. |

| Non-Immigrant B (work visa) + Thai work permit | ✅ Standard pathway | Work permit is required alongside Non-B visa. Employer relationship may help. |

| Non-Immigrant O (retirement/family) | ✅ Possible | Additional supporting documents may be requested. Some branches require extension stamps showing long stay. |

| Tourist Visa (TR) — 60 days | ⚠ Difficult | Most branches decline tourist visa holders. Some branches in tourist areas accept with additional supporting documents. Inconsistent. |

| Visa-exempt entry (30-day stamp) | ✖ Not recommended | Virtually impossible at most branches. The 30-day stamp suggests temporary visitor, not long-stay resident. |

| SMART Visa holders | ✅ Possible | SMART Visa is an official long-stay visa — most Bangkok Bank branches accept. |

| MOST PEOPLE DON’T REALIZE THIS Even within the same branch, different managers interpret the rules differently. An Indian national rejected at one branch may be accepted at another branch with the same documents. This inconsistency is a documented reality of Thai bank foreign account policies — not an error in this guide. The branch selection strategy below helps maximize your success rate. |

Account Types Available to Indian Nationals at Bangkok Bank

| Account Type | What It Is | Suitable For | Currency |

| Savings Account (basic) | Standard savings with ATM card, mobile banking | Daily local expenses, rent, utilities | THB |

| Savings Account (e-Savings) | Higher interest online savings account | Parking larger THB amounts | THB |

| Current Account | Business-style account with cheque book | Business transactions, payroll | THB |

| Fixed Deposit Account | Fixed-term savings with higher interest rate | Savings goals; requires prior savings account | THB |

| Foreign Currency Deposit (FCD) | Account in USD, EUR, GBP, or JPY | Receiving international payments without conversion; available to long-stay visa holders | USD/EUR/GBP/JPY |

For most Indian nationals in Thailand, the standard THB savings account is the starting point. Once the savings account is established, a Foreign Currency Deposit (FCD) account can be added — useful for receiving USD or EUR income without immediate THB conversion.

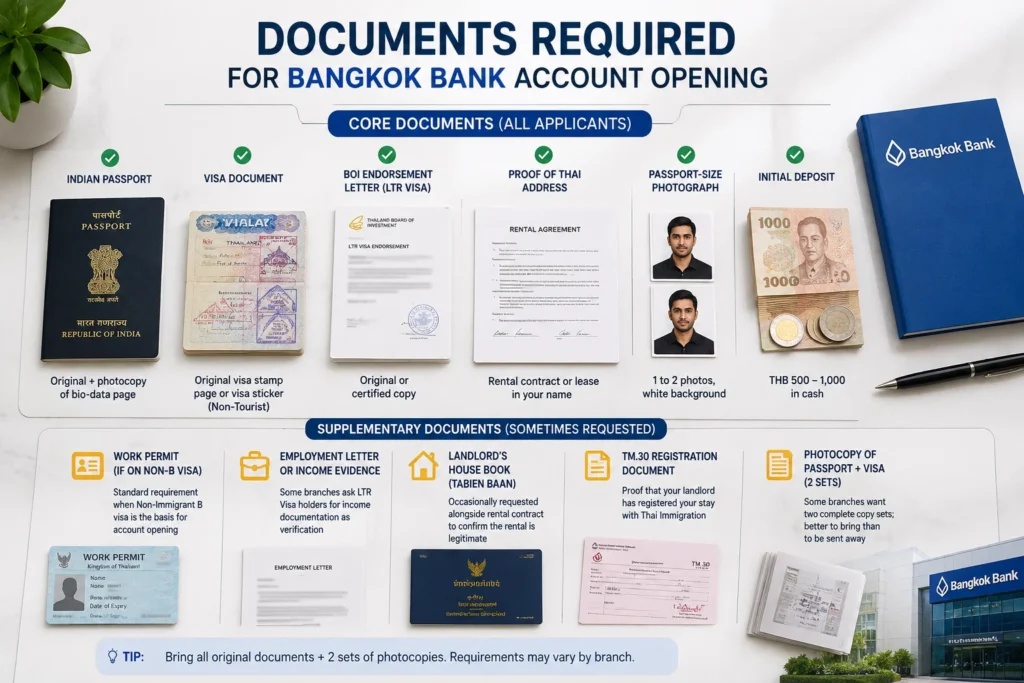

Documents Required for Bangkok Bank Account Opening

For Indian nationals, bring all of the following documents to the branch:

Core documents (all applicants)

| Document | Specification | Notes |

| Indian passport | Original + photocopy of bio-data page | Must be valid; bring original for verification |

| Visa document | Original visa stamp page or visa sticker | Type must be Non-Tourist (see visa requirements above) |

| BOI endorsement letter (LTR Visa holders) | Original or certified copy | This is your strongest eligibility document if on LTR Visa |

| Proof of Thai address | Rental contract or lease agreement in your name | Hotel booking generally not accepted; private rental or serviced apartment with contract needed |

| Passport-size photograph | 1 to 2 photos, recent, white background | Not always required but bring 2 as standard practice |

| Initial deposit | THB 500 to 1,000 in cash | Required to activate the account on opening day |

Supplementary documents (sometimes requested)

| Document | When It May Be Requested |

| Work permit (if on Non-B visa) | Standard requirement when Non-Immigrant B visa is the basis for account opening |

| Employment letter or income evidence | Some branches ask LTR Visa holders for income documentation as verification |

| Landlord’s house book (Tabien Baan) | Occasionally requested alongside rental contract to confirm the rental is legitimate |

| TM.30 registration document | Proof that your landlord has registered your stay with Thai Immigration — sometimes requested |

| Photocopy of passport + visa (2 sets) | Some branches want two complete copy sets; better to bring than to be sent away |

Bangkok Bank Account Opening: Step-by-Step Process for Indian Nationals

| STEP 1 | Choose the Right Branch Not all Bangkok Bank branches are equally comfortable serving Indian nationals. Branches in expat-heavy areas (Silom, Sukhumvit, Sathorn, Chaeng Wattana, near major coworking spaces) have more experience with foreign passport holders. The Chaeng Wattana branch near the Government Complex (Thai Immigration office area) is particularly experienced with long-stay visa holders. ⚡ Tip: Call ahead to confirm the branch accepts foreign nationals with your specific visa type. Ask: ‘Can I open an account with an LTR Visa / Non-Immigrant B visa + work permit?’ |

| STEP 2 | Prepare and Organize Your Documents Organize all documents before visiting: original passport, visa page, BOI endorsement letter (if LTR), rental contract, passport photos, and initial deposit cash. Make two photocopies of each document. Keep originals and copies in separate sections of a folder. Being organized visibly impresses branch staff and speeds the process. ⚡ Tip: Carry more documents than you think you need. It is far better to have an extra copy of your rental contract than to be sent away to photocopy something. |

| STEP 3 | Visit the Branch During Off-Peak Hours Go on weekday mornings between 9:30 AM and 11:30 AM. Avoid Monday mornings (often busy after weekend), Fridays (pre-weekend rush), and the 12:00 to 13:00 lunch period. Longer waits mean less patient staff and potentially less thorough assistance for your application. ⚡ Tip: If possible, go to a dedicated ‘foreigner services’ counter if the branch has one. Ask at the entrance if they have a counter for foreign nationals. |

| STEP 4 | Speak to a Branch Officer Request to speak with a customer service officer (not a teller) about opening a new account as a foreign national. Present your documents clearly and confidently. State your visa type upfront: ‘I have a Thailand LTR Visa’ or ‘Non-Immigrant B visa with a work permit.’ The officer will review your documents and determine eligibility. ⚡ Tip: Be patient and polite. If one officer is uncertain, politely ask to speak with the branch manager or a senior officer. This is not rude — it is practical. |

| STEP 5 | Complete the Application Form The officer will provide the account opening application form. Fill in: your name exactly as on your passport, Thai address from your rental contract, passport number, nationality (Indian), and contact details. The form is in Thai and English. If any field is unclear, ask the officer to clarify rather than guessing. ⚡ Tip: Write exactly as your passport shows. Name discrepancies cause problems later when receiving international transfers. |

| STEP 6 | Make the Initial Deposit and Receive Your Account Details After the application is approved, make the initial deposit (typically THB 500 to 1,000). The officer will provide your account number. Your ATM card is either issued immediately or mailed within 3 to 5 business days. Online banking (Bangkok Bank’s Bualuang iBanking) and mobile app (Bualuang mBanking) can be set up on the same visit. ⚡ Tip: Register for Bangkok Bank’s mobile app before leaving the branch. Their customer service team can help you set it up on the spot if needed. |

Branch Selection Strategy: Best Bangkok Bank Branches for Indian Nationals

Based on community reports from Indian nationals in Thailand, these branch types consistently perform better for foreign national account opening:

- Major branches in Silom and Sathorn area (Bangkok CBD): High volume of foreign customers; staff experienced with international documentation

- Sukhumvit Road branches (Asok, Nana, Phrom Phong area): Major expat corridor; staff familiar with non-immigrant visa holders

- Chaeng Wattana Government Complex branch: Located near Thai Immigration; staff highly experienced with LTR Visa and long-stay documentation

- Major shopping mall branches (Central World, Siam Paragon, EmQuartier, Terminal 21): Higher foot traffic from tourists and expats; more international-facing staff

- Chiang Mai: Nimman Road and Promenada Mall branches are popular with the digital nomad community

| BRANCHES TO AVOID Avoid branches in purely Thai residential neighborhoods where foreign nationals are rare. Staff in these locations are less familiar with foreign documentation requirements and more likely to decline on uncertainty rather than eligibility. Even if you qualify, the staff may not know the correct process and will default to rejection. |

Fees, Minimum Balance, and Account Features

| Feature | Standard Savings Account | Notes |

| Minimum opening deposit | THB 500 – 1,000 | Required at account opening. Verify with branch as this can vary. |

| Minimum monthly balance | THB 500 | Falling below this triggers a monthly service fee |

| Monthly service fee (if below minimum) | THB 50 per month | Avoid by maintaining THB 500+ at all times |

| ATM withdrawal fee (Bangkok Bank ATMs) | Free (Bangkok Bank ATMs only) | Use Bangkok Bank ATMs to avoid fees |

| ATM withdrawal fee (other Thai bank ATMs) | THB 20 per transaction | AEON ATMs waive fees for some account types |

| International SWIFT transfer fee (outgoing) | THB 400 to 500 + exchange rate spread | Significant cost for regular international transfers — see Wise section |

| Incoming international transfer | THB 200 per transfer + rate spread | Better received via Wise and convert to THB as needed |

| Bualuang mBanking app | Free | Full-featured mobile banking with QR Pay, PromptPay |

| iBanking (online) | Free | Web-based banking for transfers, statements, FX |

Receiving and Sending Money: Bangkok Bank SWIFT Transfers to India

Receiving income from overseas (USD/EUR to Bangkok Bank)

If your overseas employer or clients pay you via SWIFT bank transfer, you can receive USD or EUR into your Bangkok Bank account. Here is what you need to provide to the sender:

- Beneficiary bank: Bangkok Bank PCL

- SWIFT/BIC code: BKKBTHBK

- Beneficiary name: Your full name as on the account

- Beneficiary account number: Your 10-digit Bangkok Bank account number

- Branch code: Your branch’s specific code (ask the branch for this)

- Beneficiary address: Your registered Thai address

Incoming SWIFT transfers arrive in 1 to 3 business days. Bangkok Bank will convert from USD or EUR to THB using their official exchange rate, which typically has a spread of 0.5 to 1.5% away from the mid-market rate. This spread is the hidden cost of SWIFT transfers.

Sending money from Bangkok Bank to India

Bangkok Bank offers outgoing SWIFT transfers to India. To send to an Indian account (SBI, HDFC, ICICI, etc.):

- Your Indian bank’s SWIFT code (e.g., SBIN0001234 for SBI)

- IFSC code of the Indian branch (for NEFT/RTGS routing within India)

- Account holder name and account number in India

- Purpose of transfer (required by Bank of Thailand for larger amounts)

Fee: typically THB 400 to 500 per outgoing transfer, plus exchange rate spread. For transfers above THB 1,500,000 (approx. USD 42,000), Bank of Thailand reporting may apply. Keep records of large transfers.

FEMA Awareness for Indian Nationals Holding a Thai Bank Account

Indian citizens holding a bank account outside India have potential obligations under FEMA (Foreign Exchange Management Act). Key points:

- If you are classified as a Resident Indian under FEMA, you are generally not permitted to hold a foreign bank account without RBI permission

- If you qualify as a Non-Resident Indian (NRI) under FEMA — typically by spending fewer than 182 days in India in a financial year — you are permitted to hold foreign bank accounts

- Indian citizens on the Thailand LTR Visa who are spending most of the year in Thailand may qualify as NRI/PROI under FEMA, which changes their obligations regarding Indian bank accounts (converting to NRO/NRE) and foreign accounts (permitted)

- There is no automatic disclosure requirement to India’s income tax authorities for foreign bank accounts, but Schedule FA (Foreign Assets) in ITR forms requires disclosure of foreign accounts held at any time during the financial year

| IMPORTANT: CONSULT A CA BEFORE HOLDING FOREIGN ACCOUNTS FEMA compliance is complex and depends on your specific residency status and circumstances. If you are unsure whether holding a Bangkok Bank account creates FEMA obligations, consult a Chartered Accountant (CA) specializing in NRI tax and FEMA compliance before opening the account. This is not legal advice. |

Bangkok Bank vs. KBank vs. Wise: Which Is Right for You?

| Feature | Bangkok Bank | Kasikorn Bank (KBank) | Wise |

| Account opening for Indian nationals | Possible (visa dependent) | Possible (similar requirements) | Easy — fully online, no Thai visa required |

| Physical branch required | Yes | Yes | No — fully online |

| International transfers | SWIFT — THB 400–500 fee + spread | SWIFT — similar fees | Near mid-market rate; low flat fee |

| Receiving USD/EUR | SWIFT — exchange rate spread applies | SWIFT — similar | Local USD/EUR receiving accounts — no spread |

| Mobile app quality | Good (Bualuang mBanking) | Excellent (KBank app) | Excellent (Wise app) |

| PromptPay QR payments | Yes | Yes | No (local Thai QR payments not supported) |

| Local bill payments | Yes | Yes | Limited |

| Best for | Local THB expenses, rent, Thai QR pay | Local THB expenses, strong tech interface | International income, overseas payments, low-fee transfers |

The Smart Setup: Wise + Bangkok Bank for Indian Remote Workers

The most practical banking setup for Indian nationals working remotely in Thailand combines two tools for two different purposes:

| THE RECOMMENDED DUAL BANKING SETUP Wise (for international income): Use Wise to receive USD, EUR, GBP from overseas employers and clients via local bank details in each currencyConvert to THB at near mid-market rates with low fees (typically 0.4–1.5%)Transfer to your Bangkok Bank account in THB when needed for local expensesWise is fully online — no Thai visa required; Indian nationals can open via the Wise app using Indian passport and address Bangkok Bank (for local Thai expenses): Use for rent payments, utility bills, PromptPay QR transactionsLocal ATM withdrawals without foreign card feesReceiving THB from Thai local sources if neededRequired for some formal financial activities in Thailand (e.g., setting up auto-debit for utilities) Why this setup works: Wise gives you the best rates for international income; Bangkok Bank gives you full local Thai functionality. Neither is complete alone. |

Common Mistakes Indian Nationals Make When Opening Bangkok Bank Accounts

| Mistake | Why It Fails | What to Do Instead |

| Going to the nearest branch without checking foreigner experience | Random branches may lack staff who know the process for Indian passport holders | Choose branches in expat areas or those known for foreign customer service |

| Trying to open an account on a tourist visa | Bangkok Bank policy does not support tourist visa holders at most branches | Apply for LTR Visa first; use Wise as alternative until you have a qualifying visa |

| Not bringing a rental contract | Hotel booking or screenshot is not accepted as proof of address | Have a signed rental contract in your name before visiting the bank |

| Bringing only original documents without photocopies | Staff need to retain copies for KYC records | Bring 2 complete sets of photocopies for all documents |

| Expecting same-day ATM card | ATM card may be mailed to your registered address (3–5 business days) | Ask the branch about their card delivery process and confirm your address is correctly registered |

| Waiting until low on THB to apply | Account opening can take a full morning; if rejected, you need time for an alternative | Apply for your Bangkok Bank account within the first 2 weeks of arriving in Thailand with your long-stay visa |

What to Do If Your Application Is Rejected

If Bangkok Bank declines your account application, do not give up immediately. Here are your options:

- Try a different Bangkok Bank branch: The same documents can be accepted at one branch and declined at another. A branch in an expat-heavy area is more likely to accept.

- Try Kasikorn Bank (KBank): KBank has similar requirements but sometimes has different branch-level flexibility. KBank’s app is widely considered superior to Bangkok Bank’s and their international services are competitive.

- Use Wise as an interim solution: Wise can be set up from your home country (India) before arriving in Thailand using your Indian passport and address. It provides full international payment functionality without a Thai bank account.

- Wait until you have a stronger visa: If you are currently on a tourist visa and plan to apply for an LTR Visa, wait until the LTR Visa is issued before attempting a Thai bank account. The LTR endorsement letter is a significantly stronger document than a tourist visa.

- Contact Bangkok Bank’s head office: For LTR Visa holders who face rejection at branches, contacting Bangkok Bank’s head office or international customer service can sometimes resolve the issue by clarifying that LTR Visa holders are eligible customers.

Frequently Asked Questions

Can Indian nationals open a Bangkok Bank account in Thailand?

Yes, Indian nationals can open a Bangkok Bank savings account in Thailand, provided they hold a qualifying visa. LTR Visa holders (with BOI endorsement letter), Non-Immigrant B visa holders (with work permit), and Non-Immigrant O visa holders can open accounts through the standard process. Tourist visa holders and visa-exempt entry holders are typically rejected at most branches.

What documents does Bangkok Bank require from Indian nationals?

Standard documents include: Indian passport (original + copy), valid Thai visa (non-tourist), BOI endorsement letter (for LTR Visa holders), proof of Thai address (rental contract), passport-size photograph, and initial deposit (THB 500 to 1,000). Additional documents such as TM.30 registration or an employment letter may be requested depending on the branch.

Which Bangkok Bank branches are best for Indian nationals?

Branches in expat-heavy areas consistently perform better for Indian nationals: Silom, Sathorn, Sukhumvit (Asok, Phrom Phong), Chaeng Wattana (near immigration), and major shopping mall branches (Central World, Terminal 21, EmQuartier). Call ahead to confirm the branch accepts foreign nationals with your visa type before visiting.

Is it better to use Wise or Bangkok Bank for receiving international income in Thailand?

For receiving international income (USD, EUR, GBP), Wise is significantly cheaper than receiving via Bangkok Bank SWIFT transfers. Wise provides local receiving account details in each currency (e.g., a USD account number for receiving US dollar payments) and converts to THB at near mid-market rates with low fees. Bangkok Bank is better for local THB expenses, PromptPay QR transactions, and formal Thai financial activities. The recommended setup uses both.

Does holding a Bangkok Bank account create FEMA obligations for Indian nationals?

It may, depending on your Indian tax residency status. If you qualify as an NRI (Non-Resident Indian) under FEMA by spending fewer than 182 days in India in a financial year, you are permitted to hold foreign bank accounts. If you are still a Resident Indian, holding a foreign account may require RBI permission or disclosure. Schedule FA in your Indian ITR requires disclosure of foreign accounts. Consult a CA specializing in NRI and FEMA compliance for your specific situation.

Final Verdict

| Bangkok Bank remains the most internationally recognized and foreigner-accessible Thai bank for Indian nationals with qualifying visas. For LTR Visa holders, the account opening process is relatively straightforward. For Non-Immigrant visa holders with work permits, it is standard. The practical reality for Indian remote workers is that a Wise account handles international income most efficiently, while a Bangkok Bank account handles local Thai financial life. Setting up both creates a complete, cost-effective banking solution that covers all scenarios. If you do not yet have a qualifying visa, use Wise as your primary financial tool in Thailand and add a Bangkok Bank account once your LTR Visa or Non-Immigrant visa is in place. |