| The Thailand LTR Visa Wealthy Pensioner category is designed for retirees aged 50 or older who wish to reside in Thailand for up to 10 years. It offers three qualification pathways: (1) pension income of at least USD 40,000/year from passive sources such as pensions, dividends, rental income, or interest; (2) personal assets of at least USD 250,000 combined with passive income of at least USD 25,000/year; or (3) a deposit of at least USD 250,000 in a Thai bank account or Thai government bonds. Applicants must hold valid international health insurance with USD 50,000+ coverage. Employment income does not qualify under this category — only passive, retirement-type income counts. Spouses of LTR Wealthy Pensioner holders may apply as dependents regardless of their own age. The Wealthy Pensioner LTR Visa is significantly more stable than the older Thai Retirement Visa (Non-Immigrant O-A/O-X), which requires annual renewal and bank deposit maintenance. |

| QUICK ANSWER: What is the Thailand LTR Visa Wealthy Pensioner category? The LTR Visa Wealthy Pensioner category is Thailand’s long-term residence visa for retirees, offering a 10-year, multiple-entry stay. Key requirements: Age: 50 years or olderPathway 1: Passive income of USD 40,000+/year (pension, dividends, rental, interest)Pathway 2: Personal assets of USD 250,000+ AND passive income of USD 25,000+/yearPathway 3: Thai bank deposit or government bonds of USD 250,000+Health insurance: International plan with USD 50,000+ coverage valid in Thailand Unlike the older Thai Retirement Visa (Non-O-A), the LTR Wealthy Pensioner Visa is valid for 10 years with no annual bank deposit top-up requirement or annual renewal. It is the most stable legal framework for long-term retirement in Thailand. |

| DISCLAIMER This guide reflects BOI’s Wealthy Pensioner requirements as of May 2026. Requirements, income thresholds, and qualifying pathways can change. Always verify current requirements at boi.go.th before applying. This is not legal, financial, or tax advice. Consult a licensed Thai immigration attorney for your specific situation. |

Introduction

Thailand has long been a retirement destination for expats worldwide — from American retirees on Social Security and 401k income to British pensioners on State Pension and SIPPs, to Indian professionals who have retired after long careers. The combination of affordable living, excellent private healthcare, tropical climate, and a welcoming culture makes Thailand one of the world’s most practical retirement bases.

For years, the Thai Retirement Visa (Non-Immigrant O-A) was the only formal option: a visa that required annual renewal, maintaining a THB 800,000 deposit in a Thai bank account, and reporting every 90 days. It worked, but the annual administrative burden was real.

The LTR Visa Wealthy Pensioner category changes this picture entirely. Launched in 2022, it offers retirees a 10-year, multiple-entry visa with three distinct qualification pathways — designed to accommodate different income and asset profiles. This guide covers every aspect of the Wealthy Pensioner category that retirees actually need to know, including what no other guide explains: which income types qualify, which do not, and how the three qualification pathways work for different financial situations.

What Is the LTR Visa Wealthy Pensioner Category?

The Wealthy Pensioner category is one of four main categories under Thailand’s Long-Term Resident (LTR) Visa programme, administered by the Thailand Board of Investment (BOI). It is specifically designed for:

- Individuals aged 50 years or older

- Who have sufficient passive income or assets to support themselves in Thailand without working

- And who want long-term legal residence in Thailand without annual visa renewal

The category does NOT include a work permit. Wealthy Pensioner visa holders cannot be employed or perform compensated professional services in Thailand. This makes it categorically different from the Work-From-Thailand (WFT) Professional category, which is designed for remote workers who continue earning from overseas employers.

| WEALTHY PENSIONER AT A GLANCE Age requirement: 50 years or older at time of application Visa duration: 10 years, multiple entry Work authorization: None — holders may NOT work in Thailand Annual renewal: Not required (unlike Thai Retirement Visa) 90-day address report: Required (same as all LTR categories) Health insurance: USD 50,000+ international coverage required Issued by: Thailand Board of Investment (BOI), not Thai Immigration directly |

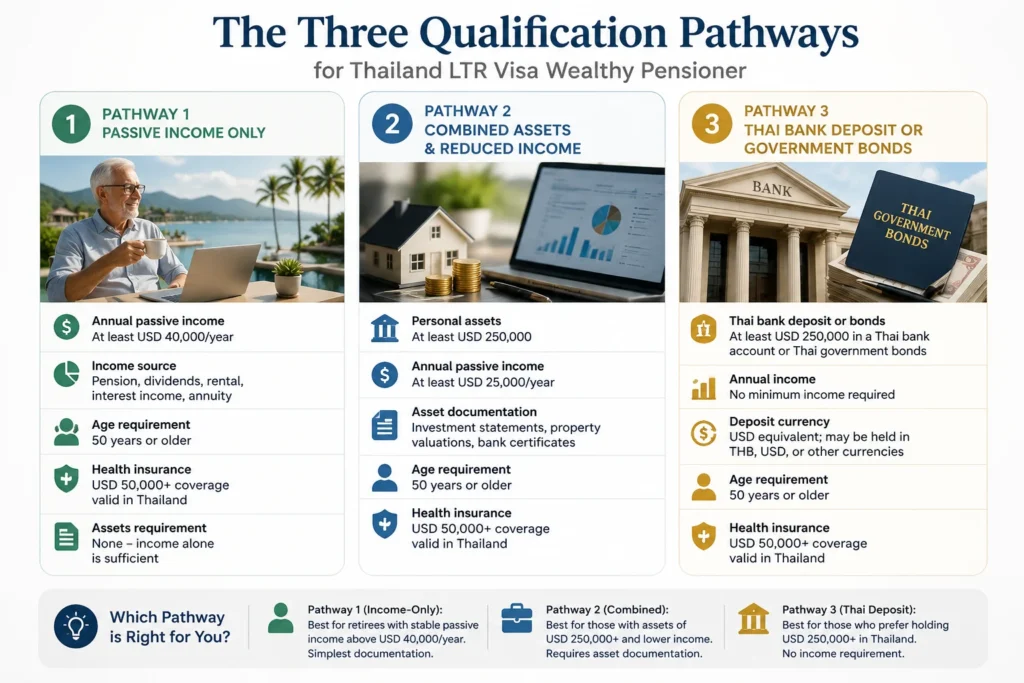

The Three Qualification Pathways for Wealthy Pensioner

This is the most important section for prospective applicants. The LTR Wealthy Pensioner category offers three distinct ways to qualify, allowing applicants with different financial profiles to meet the requirements.

Pathway 1: Passive Income Only

| Requirement | Standard |

| Annual passive income | At least USD 40,000/year from qualifying sources |

| Income source | Must be passive: pension, dividends, rental income, interest income, annuity |

| Assets requirement | None — income alone is sufficient if above threshold |

| Age requirement | 50 years or older |

| Health insurance | USD 50,000+ international coverage valid in Thailand |

This is the simplest pathway and applies to most retirees with established pension income above the threshold. Documents: pension income statements, bank statements showing 12 months of passive income credits.

Pathway 2: Combined Assets and Reduced Income

| Requirement | Standard |

| Personal assets | At least USD 250,000 (investments, securities, real estate equity, bank deposits) |

| Annual passive income | At least USD 25,000/year from qualifying sources |

| Asset documentation | Investment account statements, property valuations, bank certificates |

| Age requirement | 50 years or older |

| Health insurance | USD 50,000+ international coverage valid in Thailand |

This pathway is designed for asset-rich retirees whose ongoing income is below USD 40,000/year but who have substantial savings or investments. A retiree with USD 500,000 in an investment portfolio earning USD 25,000/year in dividends qualifies under this pathway.

Pathway 3: Thai Bank Deposit or Government Bonds

| Requirement | Standard |

| Thai bank deposit or bonds | At least USD 250,000 deposited in a Thai commercial bank account OR invested in Thai government bonds |

| Annual income | No minimum income required under this pathway |

| Deposit currency | USD equivalent; may be held in THB, USD, or other currencies at a Thai bank |

| Age requirement | 50 years or older |

| Health insurance | USD 50,000+ international coverage valid in Thailand |

This pathway is the most straightforward for those with significant liquid savings: deposit USD 250,000+ into a Thai bank account or purchase Thai government bonds of equivalent value, and the income requirement is waived entirely.

| WHICH PATHWAY IS RIGHT FOR YOU? Pathway 1 (income-only): Best for retirees with established, consistent passive income above USD 40,000/year from pensions, dividends, or rental income. Simplest documentation. Pathway 2 (combined): Best for retirees with significant investments or property equity (USD 250,000+) who are drawing less than USD 40,000/year from those assets. Requires asset documentation. Pathway 3 (Thai deposit): Best for retirees who prefer to hold significant liquid savings in Thailand and eliminate the income documentation requirement entirely. Requires maintaining the deposit. |

Qualifying Income Types: What Counts Under Wealthy Pensioner

Under Pathways 1 and 2, income must be passive in nature. The following qualify:

| Income Type | Qualifies? | Examples |

| State / government pension | ✅ Yes | US Social Security, UK State Pension, Indian government pension, Australian Age Pension |

| Private / occupational pension | ✅ Yes | UK SIPP, US 401k distributions, Canadian RRSP, Indian EPFO pension, NPS annuity |

| Annuity income | ✅ Yes | Life insurance annuity (LIC, AIA, MetLife), fixed annuity payments |

| Dividend income | ✅ Yes | Dividends from shares, mutual funds, ETFs, REITs |

| Rental income | ✅ Yes | Income from renting out property (anywhere in the world) |

| Interest income | ✅ Yes | Bank interest, bond coupon payments, fixed deposit returns |

| Investment income (distributions) | ✅ Yes | Regular distributions from managed funds, unit trusts |

| Employment income | ❌ No | Salary, consulting fees, freelance income, business revenue |

| Capital gains (irregular) | ❌ Not consistently | One-off capital gains are not considered stable passive income by BOI |

| Business profits | ❌ No | Active business income does not qualify under Wealthy Pensioner |

| CRITICAL: EMPLOYMENT INCOME DOES NOT QUALIFY Many retirees who still do some consulting, advisory work, or part-time employment assume this income can count toward the Wealthy Pensioner threshold. It cannot. The Wealthy Pensioner category is explicitly for passive retirement income. If your USD 40,000+ income includes employment or consulting fees, you should consider the Work-From-Thailand (WFT) Professional category instead — even if you are aged 50+. A retiree who earns USD 20,000 in pension and USD 25,000 in consulting fees does NOT qualify for Wealthy Pensioner (total is above USD 40,000, but the consulting income is disqualified). They may qualify for WFT Professional if the combined employment/freelance income meets that category’s requirements. |

Documents Required for LTR Wealthy Pensioner Application

| Document | What It Shows | Source |

| Passport | Identity, age (must be 50+), nationality | Current, valid national passport |

| Age proof | Confirms applicant is 50+ years old | Passport bio-data page (date of birth) |

| Pension / income statements | Confirms passive income level and source | Pension administrator, fund manager, or financial institution letter |

| Bank statements (12 months) | Shows passive income deposits and pattern | Home country bank or Thai bank showing 12 months of income credits |

| Asset documentation (Pathway 2 only) | Confirms assets of USD 250,000+ | Investment account statements, property valuation, bank certificates |

| Thai bank deposit certificate (Pathway 3 only) | Confirms USD 250,000+ in Thai bank | Thai bank certificate of deposit issued in USD equivalent |

| International health insurance certificate | Confirms USD 50,000+ Thailand coverage | Insurer’s formal certificate (not an app screenshot or card) |

| Passport-size photographs | ID photos for application | Recent, white background |

Step-by-Step Application Process

- Determine your qualification pathway: income-only, combined, or Thai deposit

- Gather income documentation: 12 months of bank statements showing passive income, pension statements, and investment reports

- Arrange qualifying health insurance: Purchase an international plan (Cigna Global, AXA International, Allianz Care, Bupa Global) with USD 50,000+ Thailand coverage. Ensure you pass underwriting — pre-existing conditions may affect coverage terms

- Prepare asset documentation if using Pathway 2: Investment account statements showing USD 250,000+ in personal assets

- Open Thai bank account and make deposit if using Pathway 3: Open account with Bangkok Bank or KBank, transfer USD 250,000+ equivalent, and obtain bank certificate

- Register on BOI portal: Create account at ltrvisat.boi.go.th

- Submit application online: Complete the Wealthy Pensioner category application, upload all documents, and pay the THB 50,000 non-refundable endorsement fee

- Wait for BOI review: 20 to 35 working days. Monitor email for Additional Information Requests (AIR)

- Receive BOI endorsement letter

- Book appointment at Royal Thai Embassy or Consulate in your home country and pay the THB 10,000 visa stamp fee

- Travel to Thailand and activate your LTR Visa on first entry

Cost Breakdown for Wealthy Pensioner LTR Visa

| Cost Item | Amount (USD approx.) | Notes |

| BOI endorsement fee | USD 1,395 (THB 50,000) | Non-refundable. Paid online. |

| Visa stamp fee (Thai Embassy/Consulate) | USD 280 (THB 10,000) | Paid at Thai Embassy in your country. |

| International health insurance (annual) | USD 1,000–2,500+/year for 50+ | Increases with age. Pre-existing conditions affect availability and premium. |

| Asset documentation / bank certificates | USD 0–300 | Usually low-cost from financial institution. |

| TOTAL first year (excluding insurance) | Approx. USD 1,675–1,700 | Insurance adds USD 1,000–2,500+ annually. |

Note: For Pathway 3 (Thai bank deposit), the USD 250,000 deposit is not a fee — it is your own money in a Thai bank account. It earns interest and can be withdrawn if you leave Thailand permanently. Factor in the opportunity cost of this capital relative to your home country investment returns.

LTR Wealthy Pensioner vs Thai Retirement Visa: Full Comparison

Most retirees considering Thailand already know about the older Thai Retirement Visa (Non-Immigrant O-A). Here is the complete comparison with the LTR Wealthy Pensioner category:

| Factor | LTR Wealthy Pensioner | Thai Retirement Visa (Non-O-A/O-X) |

| Minimum age | 50 years | 50 years |

| Visa duration | 10 years, multiple entry | 1 year (O-A) or 10 years (O-X, for USD 80K deposit) |

| Annual renewal | Not required | Required every year (O-A) |

| Income requirement | USD 40,000/year passive income | THB 65,000/month income (approx. USD 23,000/year) |

| Bank deposit (Thai) | Optional — USD 250,000 for Pathway 3 | Required: THB 800,000 (∼USD 22,000) maintained in Thai bank |

| Health insurance | USD 50,000+ international required | Required (lower threshold than LTR) |

| Work authorization | None | None |

| BOI involvement | Yes — BOI endorsement + Embassy stamp | Thai Immigration only — no BOI |

| Re-entry permits | Not required (multiple entry) | Required if exiting Thailand (O-A) |

| 90-day address report | Required | Required |

| Application complexity | Higher (BOI portal + Embassy) | Lower (Thai Immigration or consulate only) |

| One-time visa cost | THB 63,800 (∼USD 1,775) | THB 2,000 (O-A) or higher (O-X) |

| Best for | High-income retirees who want 10-year stability | Retirees meeting lower Thai deposit/income thresholds; or those not meeting LTR income level |

| WHICH IS BETTER: LTR OR THAI RETIREMENT VISA? The LTR Wealthy Pensioner is generally better for retirees who: Have passive income clearly above USD 40,000/yearWant to avoid annual renewal bureaucracyAre comfortable with the higher one-time cost in exchange for 10-year stabilityWant multiple-entry freedom without re-entry permits The Thai Retirement Visa (Non-O-A) may be better for retirees who: Have passive income of USD 23,000–39,000/year (above Thai requirement but below LTR threshold)Prefer a lower upfront cost despite annual renewalAre comfortable maintaining THB 800,000 in a Thai bank |

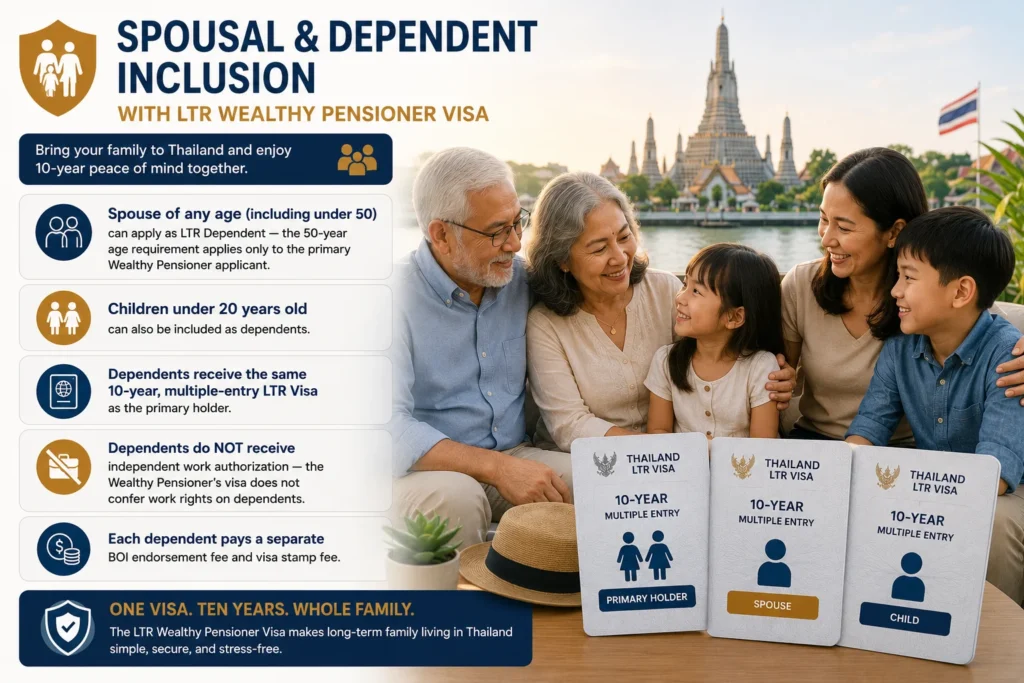

Spousal and Dependent Inclusion

LTR Wealthy Pensioner holders can include their spouse and children as dependents on a separate but linked LTR Dependent Visa. Key points:

- Spouse of any age (including under 50) can apply as LTR Dependent — the 50-year age requirement applies only to the primary Wealthy Pensioner applicant

- Children under 20 years old can also be included as dependents

- Dependents receive the same 10-year, multiple-entry LTR Visa as the primary holder

- Dependents do NOT receive independent work authorization — the Wealthy Pensioner’s visa does not confer work rights on dependents

- Each dependent pays a separate BOI endorsement fee and visa stamp fee

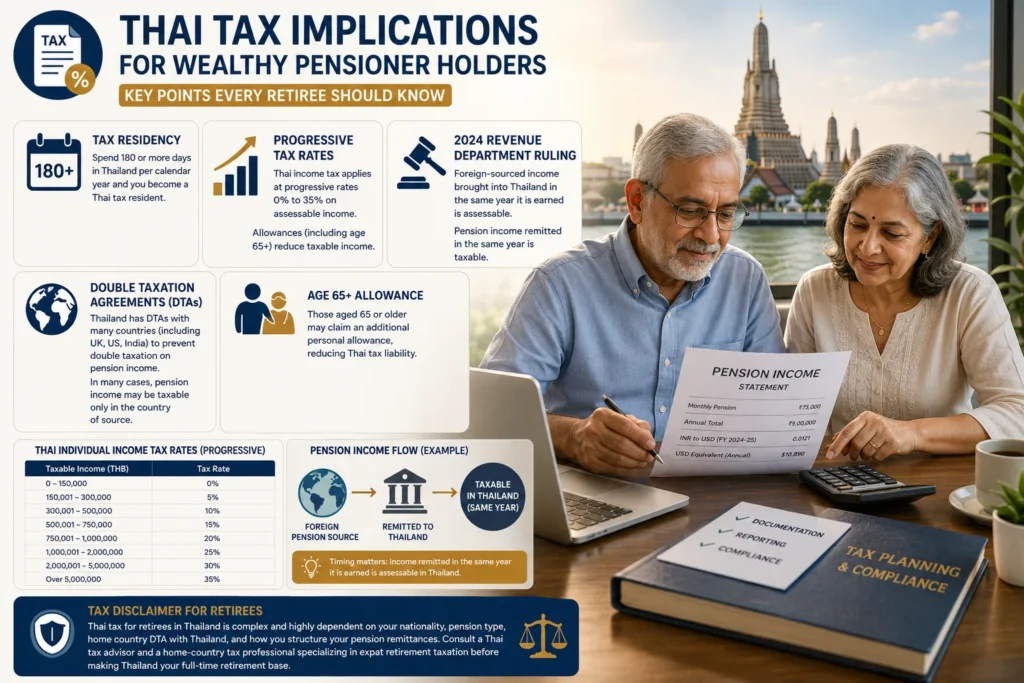

Thai Tax Implications for Wealthy Pensioner Holders

Retirees who spend 180 or more days in Thailand per calendar year become Thai tax residents. For pensioners, the relevant tax implications:

- Thai income tax applies at progressive rates (0% to 35%) on assessable income. The personal allowance and allowances for age (additional allowance for those aged 65+) reduce taxable income

- The 2024 Revenue Department ruling (Phor Ngor 161/2566) clarified that foreign-sourced income brought into Thailand in the same year it is earned is assessable. Pension income remitted to Thailand from a foreign pension in the same year is taxable under this ruling

- Pension income from foreign pension funds: Thailand’s DTAs with many countries (including the UK, US, and India) typically provide provisions on which country has taxing rights on pension income. In many cases, pension income may be taxable only in the country of source, or the DTA provides a mechanism to avoid double taxation

- Thai personal allowances for 65+: Those aged 65 or older may claim an additional personal allowance, reducing Thai tax liability

| TAX DISCLAIMER FOR RETIREES Thai tax for retirees in Thailand is complex and highly dependent on your nationality, pension type, home country DTA with Thailand, and how you structure your pension remittances. Do not rely on general forum advice for your retirement tax planning. Consult a Thai tax advisor and a home-country tax professional specializing in expat retirement taxation before making Thailand your full-time retirement base. |

Nationality-Specific Guidance: Indian Pensioners

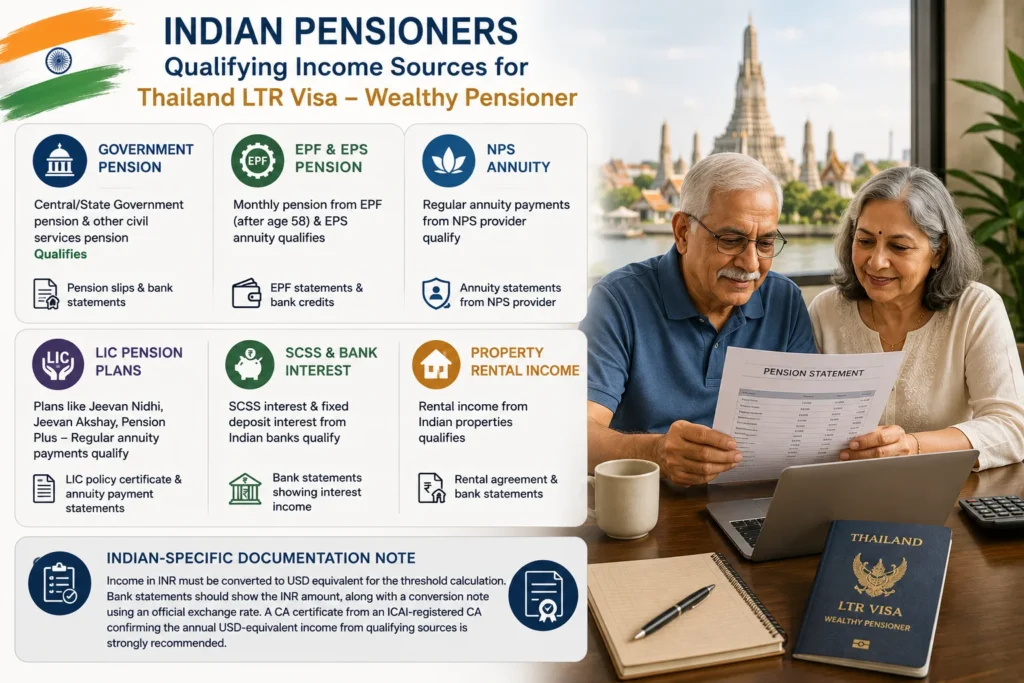

| INDIA-SPECIFIC WEALTHY PENSIONER GUIDANCE Indian retirees have several pension types that qualify under the Wealthy Pensioner income requirement: Government pension / Central Civil Services pension: Qualifies. Pension slips and bank statements showing monthly pension credits are the documentation. Employee Provident Fund (EPF) distributions: Regular monthly pension from the EPF (after age 58) qualifies. EPS (Employee Pension Scheme) annuity counts as qualifying income. National Pension System (NPS) annuity: Regular annuity payments from NPS annuity provider (LIC, Bajaj Allianz, SBI Life, etc.) qualify. Lump sum NPS withdrawal does NOT qualify as regular income.LIC pension plans (Jeevan Nidhi, Jeevan Akshay, Pension Plus): Regular annuity payments qualify. Document with LIC policy certificate and annuity payment statements. Senior Citizen Savings Scheme (SCSS) and interest: SCSS interest income qualifies. Fixed deposit interest from Indian banks qualifies. Property rental income from India: Rental income from Indian properties received regularly qualifies if above the threshold (with currency conversion context). Indian-specific documentation note: Income in INR must be converted to USD equivalent for the threshold calculation. The bank statement should show the INR amount, and you should provide a conversion note using an official exchange rate. A CA certificate from an ICAI-registered CA confirming the annual USD-equivalent income from qualifying sources is strongly recommended for Indian Wealthy Pensioner applicants. |

Health Insurance: The Age Factor for Pensioner Applicants

Health insurance is a more complex consideration for the Wealthy Pensioner category than for the WFT Professional category, for two reasons: age-related premium increases and pre-existing conditions.

Age-related premium increases

International health insurance premiums increase with age. A 60-year-old applicant pays approximately 2 to 3 times more than a 40-year-old for equivalent coverage. A 70-year-old may pay 4 to 5 times more. Budget accordingly when calculating the true annual cost of the LTR Wealthy Pensioner category over a 10-year horizon.

Pre-existing conditions

Insurers may exclude pre-existing conditions (diabetes, hypertension, cardiac conditions, cancer history) from the USD 50,000+ coverage. A policy that technically provides USD 50,000 in coverage but excludes your main health concern is not practically useful. Read the policy exclusions carefully.

| Insurer | Age Availability | Pre-Existing Condition Policy |

| Cigna Global | Up to 74 at entry | Medical underwriting; conditions may be excluded or covered with premium loading |

| AXA International | Up to 74 at entry | Similar to Cigna; exclusion or premium loading for declared conditions |

| Allianz Care | Up to 69 at entry (new) | Medical underwriting; comprehensive coverage for healthy applicants |

| Bupa Global | Up to 75 at entry | Full medical underwriting; exclusions possible for declared conditions |

| Pacific Cross (Thailand-based) | No upper age limit for renewals | Thailand-based insurer familiar with Thai healthcare; available from local Thai brokers |

Common Mistakes Pensioner Applicants Make

| Mistake | Consequence | Prevention |

| Including consulting or employment income in the USD 40,000 threshold calculation | Disqualified from Wealthy Pensioner category; may need to apply under WFT Professional instead | Calculate threshold using passive income only (pension, dividends, rental, interest) |

| Not accounting for currency conversion in income assessment | Pension income in INR, GBP, or AUD may fluctuate above and below the USD threshold with exchange rate movements | Use 12-month bank statements plus a currency conversion note; consider if your USD-equivalent income is consistently above threshold |

| Buying a health insurance policy without checking pre-existing condition coverage | Policy may exclude your main health concern despite meeting the USD 50,000 face value requirement | Get full policy terms before purchasing; use a Thailand health insurance broker to compare options |

| Pathway 3 applicants not opening Thai bank account before application | Cannot document the Thai deposit until account is opened; adds weeks to timeline | Open Bangkok Bank or KBank account and make the deposit before starting the BOI portal application |

| Assuming LTR Visa means no 90-day address reporting | LTR Wealthy Pensioner holders must still report their address every 90 days to Thai Immigration | Set a calendar reminder every 85 days to report address at Immigration or online |

Risks and Limitations

- Income floor risk: If your passive income falls below the threshold due to investment losses, reduced dividends, or pension restructuring, your LTR Visa qualification may be at risk at renewal or investigation. Maintain a buffer above the threshold.

- No work authorization: Wealthy Pensioner holders cannot work, consult, or receive any compensation for professional services in Thailand. If you later want to return to paid work, you would need to apply under the WFT Professional category.

- Thai bank deposit lock-in (Pathway 3): The USD 250,000 deposit must be maintained. Withdrawing below the threshold while on the visa could create compliance issues.

- Health insurance cost escalation: As you age through the 10-year visa period, health insurance premiums will increase significantly. Build this cost escalation into your retirement income planning.

- Tax implications: Spending 180+ days in Thailand creates Thai tax residency. Pension income remitted to Thailand in the same year it is earned may be subject to Thai income tax. Plan accordingly.

Frequently Asked Questions

What is the Thailand LTR Visa Wealthy Pensioner category?

The LTR Visa Wealthy Pensioner category is Thailand’s 10-year long-term residence visa for retirees aged 50 or older. It requires passive income of at least USD 40,000/year (Pathway 1), or personal assets of USD 250,000+ with income of USD 25,000+/year (Pathway 2), or a Thai bank deposit of USD 250,000+ (Pathway 3). It includes valid international health insurance and no work authorization.

What income types qualify for Wealthy Pensioner LTR Visa?

Qualifying income includes state pensions, private/occupational pensions, annuities, dividends, rental income, and bank interest. Employment income, consulting fees, and active business income do NOT qualify. Only passive, retirement-type income counts toward the threshold.

How is the LTR Wealthy Pensioner visa different from the Thai Retirement Visa?

The LTR Wealthy Pensioner requires higher income (USD 40,000/year vs approximately USD 23,000/year for Thai Retirement Visa) but provides 10 years of multiple-entry validity without annual renewal, no mandatory Thai bank deposit for Pathways 1 and 2, and no re-entry permit requirement. The Thai Retirement Visa (Non-O-A) has lower income requirements but requires annual renewal and maintaining THB 800,000 in a Thai bank.

Can my spouse come with me on the LTR Wealthy Pensioner visa?

Yes. Spouses of LTR Wealthy Pensioner holders can apply for an LTR Dependent Visa, which provides the same 10-year, multiple-entry validity. The spouse does not need to be aged 50+ — the age requirement applies only to the primary applicant. Dependent applicants pay separate BOI endorsement and visa stamp fees.

Does Indian EPF or NPS pension count toward the Wealthy Pensioner threshold?

Yes. Regular monthly annuity from the Employee Pension Scheme (EPS under EPF) and regular NPS annuity payments from a registered annuity provider qualify as passive pension income. One-time NPS lump sum withdrawal does not qualify as recurring income. Document with pension payment slips and bank statements showing 12 months of regular deposits, plus a CA certificate from an ICAI-registered CA confirming the annual USD equivalent.

Final Verdict: Is the LTR Wealthy Pensioner Category Right for You?

| The LTR Wealthy Pensioner category is the most stable and dignified long-term retirement visa option Thailand offers. For retirees who meet the income or asset thresholds, it eliminates the annual renewal stress, bank deposit maintenance, and re-entry permit requirements of the old Thai Retirement Visa. The three qualification pathways make it genuinely flexible: income-only, combined assets, or Thai deposit. One of these pathways is likely a match for most retirees who are seriously planning long-term Thailand retirement. The health insurance requirement and cost escalation with age are the most important practical considerations. Plan your insurance costs for years 5 to 10, not just year 1, to ensure the visa remains financially manageable throughout its 10-year validity. If your passive income clearly exceeds USD 40,000/year and you want 10 years of legally certain, hassle-free retirement residence in Thailand: the Wealthy Pensioner category is the correct choice. |