| Wise for digital nomads: Wise (formerly TransferWise) is an FCA-regulated UK fintech company offering multi-currency accounts, international transfers at mid-market exchange rates, and a global debit card. For digital nomads, Wise solves the most expensive problem in international money management: currency conversion markup. Traditional banks charge 2% to 5% above the mid-market rate; Wise charges a transparent fee (typically 0.4% to 1.5% depending on currency corridor) plus the actual mid-market rate. Wise supports 40+ currencies with local bank account details in major markets (USD routing number, UK sort code, EU IBAN, Australian BSB). The Wise debit card (Mastercard) includes 2 free ATM withdrawals per month up to your plan’s limit. Wise does not support Thai baht (THB) as a holding currency, making it a transfer and conversion tool rather than a local account for Thailand-based nomads. For Indian digital nomads: Wise works well for sending overseas income to Indian NRE/NRO accounts. For Filipino nomads: transfers to BDO, BPI, and Union Bank work directly; GCash wallet top-up also available through Remitly partnership. |

| QUICK ANSWER: Is Wise good for digital nomads? Yes — Wise is one of the best international money management tools for digital nomads. Key reasons: Mid-market exchange rate: No markup on the exchange rate itself; only a transparent, low feeMulti-currency account: Hold, send, and receive in 40+ currenciesLocal bank details: US routing number, UK sort code, EU IBAN, AUS BSB for receiving income like a localWise debit card: Works globally; 2 free ATM withdrawals per monthIndia and Philippines: Works well for sending overseas income to INR and PHP bank accounts Limitation: Wise does not hold Thai baht (THB). Thailand-based nomads use Wise as a conversion and transfer tool, not as their primary Thai account. |

| AFFILIATE DISCLOSURE This article contains affiliate links. If you open a Wise account using our link, MeridianNomad may receive a commission at no extra cost to you. Our review reflects genuine experience and research — Wise is a tool we recommend because it is genuinely the best for most nomad international money situations, not because of the affiliate arrangement. All fee data is sourced from Wise’s official pricing page (wise.com/pricing). |

What Is Wise?

Wise was founded in 2011 in London as TransferWise, built on a simple premise: the foreign exchange ‘spread’ that banks charge when converting currencies is a hidden fee that most customers don’t notice until they calculate how much they actually received. The solution: use the real mid-market rate (the rate you see on Google) and charge only a transparent, upfront fee for the service.

Rebranded as Wise in 2021, the company now serves 16+ million customers globally, is regulated by the FCA (UK Financial Conduct Authority), and has expanded beyond transfers into a full multi-currency account with local bank details and a debit card. It is not a bank — it is an e-money institution — but for international money management, it serves more of the functions that digital nomads need than most traditional banks.

Wise Key Features for Digital Nomads

| Feature | What It Does | Why Nomads Need It |

| Multi-currency account | Hold money in 40+ currencies simultaneously | Manage USD client income, EUR Europe spending, THB Thailand costs in one place |

| Local bank details | Get US routing number, UK sort code, EU IBAN, AUS BSB, SGD, CAD, NZD bank details | Receive overseas client payments as if you have a local bank account in their country |

| Mid-market rate transfers | Send money between currencies at the real exchange rate + small transparent fee | Save 2–5% vs traditional bank conversion on every international transfer |

| Wise debit card | Mastercard debit card that works in 175+ countries | Pay at local merchants and ATMs wherever you are; auto-converts from your best-rate balance |

| Batch payments | Send up to 1,000 payments in one upload (Business) | Useful for nomads with sub-contractors or multiple recurring payments |

| Wise Business account | Separate account for business payments with invoicing | Useful for freelancers who want to separate business and personal income |

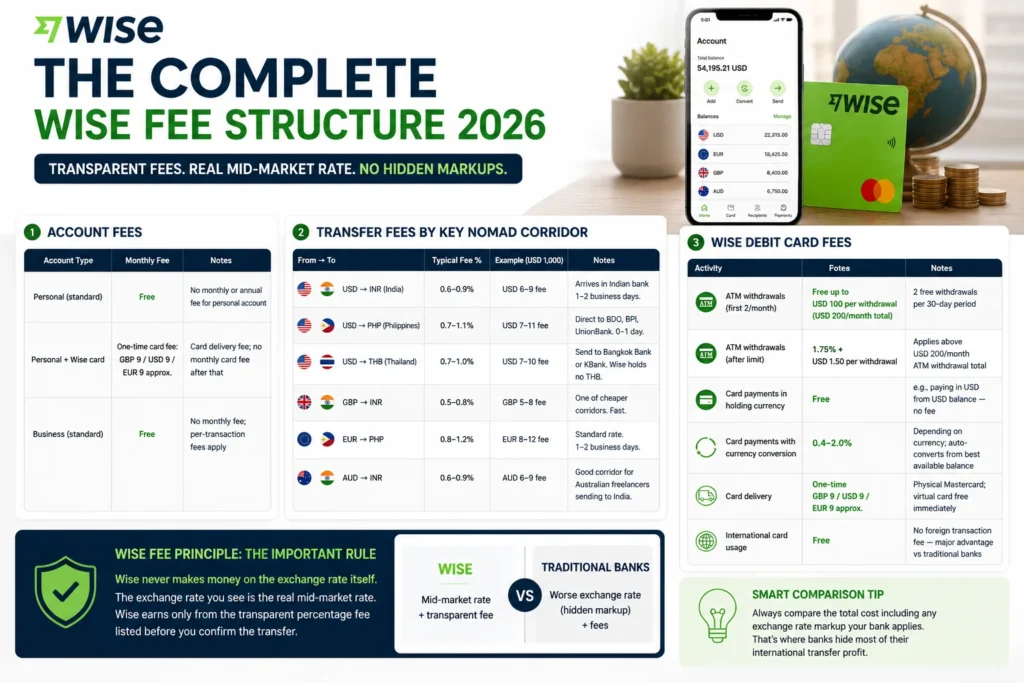

The Complete Wise Fee Structure 2026

Wise’s transparency on fees is one of its strongest differentiators. Here is the complete fee breakdown as of 2026:

Account fees

| Account Type | Monthly Fee | Notes |

| Personal (standard) | Free | No monthly or annual fee for personal account |

| Personal + Wise card | One-time card fee: GBP 9 / USD 9 / EUR 9 approx. | Card delivery fee; no monthly card fee after that |

| Business (standard) | Free | No monthly fee; per-transaction fees apply |

Transfer fees by key nomad corridor

| From → To | Typical Fee % | Example (USD 1,000) | Notes |

| USD → INR (India) | 0.6–0.9% | USD 6–9 fee | Mid-market rate + fee. Arrives in Indian bank 1–2 business days. |

| USD → PHP (Philippines) | 0.7–1.1% | USD 7–11 fee | Direct to BDO, BPI, UnionBank. 0–1 business day. |

| USD → THB (Thailand) | 0.7–1.0% | USD 7–10 fee | Send to Bangkok Bank or KBank. Wise holds no THB. |

| GBP → INR | 0.5–0.8% | GBP 5–8 fee | One of cheaper corridors. Fast. |

| EUR → PHP | 0.8–1.2% | EUR 8–12 fee | Standard rate. 1–2 business days. |

| AUD → INR | 0.6–0.9% | AUD 6–9 fee | Good corridor for Australian freelancers sending to India. |

Wise debit card fees

| Activity | Fee | Notes |

| ATM withdrawals (first 2/month) | Free up to USD 100 per withdrawal (USD 200/month total) | 2 free withdrawals per 30-day period |

| ATM withdrawals (after limit) | 1.75% + USD 1.50 per withdrawal | Applies above USD 200/month ATM withdrawal total |

| Card payments in holding currency | Free | e.g., paying in USD from USD balance — no fee |

| Card payments with currency conversion | 0.4–2.0% depending on currency | Auto-converts from best available balance |

| Card delivery | One-time GBP 9 / USD 9 / EUR 9 approx. | Physical Mastercard; virtual card free immediately |

| International card usage | Free (no foreign transaction fee) | One of Wise’s major advantages vs traditional bank cards |

| WISE FEE PRINCIPLE: THE IMPORTANT RULE Wise never makes money on the exchange rate itself. The exchange rate you see is the real mid-market rate. Wise earns only from the transparent percentage fee listed before you confirm the transfer. This is different from most banks, which give you a worse exchange rate and call it ‘no fee.’ When comparing Wise to your bank: don’t compare just the stated fees. Calculate the total cost including any exchange rate markup your bank applies. The exchange rate markup is where banks hide most of their international transfer profit. |

Wise Multi-Currency Account: How It Works

The Wise multi-currency account is what makes Wise more than a transfer service. With a Wise personal account, you can:

- Hold over 40 currencies simultaneously in separate currency ‘jars’

- Get local bank account details in the US (routing + account number), UK (sort code + account), EU (IBAN), Australia (BSB + account), Canada (institution + transit + account), Singapore (bank + account), New Zealand, and more

- Receive bank transfers as if you are a local in those countries — useful for receiving US client payments without international wire fees

- Convert between currencies in the account at mid-market rate + fee

How nomads use local bank details

A common nomad workflow: tell your US-based client to pay you via ACH transfer to your Wise US account details (routing + account number). They pay a domestic US transfer (no international fee). The money arrives in your Wise USD balance. You convert to INR, PHP, or THB at mid-market rate and send to your local bank. This eliminates the international wire fee your client would otherwise pay — and removes any receiving fee from your home bank.

Wise Debit Card: Features, ATM Policy, and Real-World Nomad Use

The Wise debit card is a physical Mastercard that works at any merchant or ATM that accepts Mastercard globally. It is one of the best travel cards available for three reasons: no foreign transaction fee, mid-market rate on purchases, and 2 free ATM withdrawals per month.

How the card converts currency at payment

When you pay in a currency you hold in your Wise account, it uses that balance directly (no conversion). When you pay in a currency you do not hold, Wise auto-converts from your largest-balance currency at mid-market rate + the applicable conversion fee. The card automatically selects the best balance to convert from to minimize fees.

ATM policy in practice

- 2 free ATM withdrawals per 30-day period up to USD 100 each (USD 200 total free per month)

- After the free limit: 1.75% + USD 1.50 (or local currency equivalent) per withdrawal

- At Thailand ATMs: Thai ATMs charge their own withdrawal fee (typically THB 200 to 250, approximately USD 6) regardless of Wise’s fee structure. Use the Wise card for purchases rather than ATM withdrawals in Thailand to avoid the Thai bank fee.

- At India ATMs: Some Indian ATMs accept foreign Mastercards; Wise card works at VISA/Mastercard-branded ATMs

- At Philippines ATMs: Works at most BancNet and Plus/Cirrus ATMs

Wise for Indian Digital Nomads: Complete Guide

| INDIA-SPECIFIC WISE GUIDE Wise is fully operational in India. Key India-specific information: Receiving income in India via Wise: Use your Wise USD/EUR/GBP account details to receive overseas client paymentsTransfer from Wise to your Indian NRE account: Wise → NRE bank account (HDFC, ICICI, SBI, etc.) via SWIFT or local transfer. Mark as ‘foreign income repatriation.’Transfer to NRO account: for India-sourced income or mixed fundsFIRC (Foreign Inward Remittance Certificate): Your Indian bank issues FIRC/eBRC when you receive international transfers. Wise transfers qualify as foreign remittances and generate FIRC documentation from your Indian bank. Key India limitations: Wise does not offer an INR account (you cannot hold rupees in Wise). Send to Indian bank as conversion transaction.LRS (Liberalised Remittance Scheme): Sending money OUT of India via Wise is subject to RBI’s LRS limit (USD 250,000/year per individual). Sending into India has no outward LRS cap from Wise’s side.TCS (Tax Collected at Source): From 2023, sending money from India abroad above INR 7 lakh/year under LRS attracts TCS. This does not affect overseas income coming INTO India via Wise. India Wise fee example: USD 5,000 sent from Wise USD to HDFC NRE INR: approximately USD 35–45 in Wise fees + INR 500–1,500 SWIFT fee from Indian bank (on top of Wise fee). Total cost significantly less than traditional USD bank wire. |

Wise for Filipino Digital Nomads: Complete Guide

| PHILIPPINES-SPECIFIC WISE GUIDE Wise works well for Filipino digital nomads. Key Philippines-specific information: Receiving client payments via Wise: Use Wise USD account details (routing + account) for US client paymentsUse Wise EUR details for EU client paymentsTransfer from Wise to Philippine banks: BDO, BPI, Metrobank, UnionBank, Landbank, PNB — all supported for direct transfers GCash: Wise to GCash: Not always direct. Check Wise’s current Philippine transfer options. Some users route via GCash’s bank account details (Maya / GCash has a backend bank account). Remitly as an alternative specifically supports GCash mobile wallet delivery from overseas. Wise USD → PHP transfer fee: typically 0.7–1.1%. On USD 1,000: approximately PHP 70–110 equivalent. Compare: Western Union charges PHP 300–800 for similar amount. Philippine BIR considerations: Overseas income received in the Philippines via Wise transfers counts as foreign-sourced income. Filing obligations depend on BIR residency status. Consult a Philippine CPA for ITR implications of regular international wire receipts. Wise card in the Philippines: Works at ATMs accepting Visa/Mastercard/Plus. Philippine ATMs also charge withdrawal fees (typically PHP 200–250 per withdrawal). Use card for purchases at merchants accepting Mastercard to avoid ATM fees. |

Wise for Thailand-Based Nomads: The THB Limitation

This is the most important Thailand-specific piece of information that most Wise reviews skip: Wise does not support Thai baht (THB) as a currency you can hold in your Wise account.

What this means in practice

- You cannot receive THB directly into a Wise account

- You cannot hold THB in Wise or use a Wise account as your primary Thai bank account

- You CAN send USD/EUR/GBP from Wise to a Thai bank account (Bangkok Bank or KBank) with THB conversion happening at the Thai bank side

The recommended Thailand + Wise setup

| THAILAND-BASED NOMAD BANKING SETUP Primary Thai account: Bangkok Bank or KBank (opened with LTR Visa BOI letter or SMART Visa) Wise role: International income reception and conversion tool Workflow: Step 1: US/EU client pays into your Wise USD/EUR account details Step 2: In Wise: Convert USD/EUR to THB and send to Bangkok Bank Step 3: Bangkok Bank receives THB directly; you spend from Bangkok Bank in Thailand Step 4: For India: Convert USD to INR in Wise and send to NRE/NRO account Step 5: Use Wise card for international purchases or countries where you don’t have local banking This setup gives you local Thai banking (Bangkok Bank) for daily life in Thailand + Wise for international income management. The two together cover everything a Thailand-based nomad needs. |

Setting Up Wise: Step-by-Step Guide

- Go to wise.com or open the Wise app (iOS/Android). Click ‘Register’ and choose Personal or Business account.

- Sign up with your email address or Google account. Set a strong password.

- Verify your identity: Upload a passport photo (front page) + take a real-time selfie. Wise’s verification is typically instant or within a few hours. Accepted: Passport, national ID card, driving licence (country-dependent).

- Add a currency and get local bank details: Go to ‘Home’ → ‘Open a balance’ → Select USD. You immediately get your US routing number and account number. Repeat for GBP, EUR, AUD, CAD as needed.

- Add money: Bank transfer (cheapest), debit card, or credit card (higher fee). First transfer from a bank account is recommended to keep costs minimal.

- Order your Wise card: ‘Card’ section in the app. Pay the one-time card fee (GBP 9 / USD 9 equivalent). Delivery in 1 to 3 weeks depending on your country. Virtual card is available immediately for online purchases.

- Set up transfer to your home bank: For India: Add NRE/NRO account details (IFSC + account number). For Philippines: Add BDO/BPI/UnionBank details. Test with a small amount first.

- Share your local bank details with clients: For US clients, share your Wise USD routing + account number. They send a domestic ACH (no international fee for them). You receive in your Wise USD balance.

Wise vs Payoneer: The Freelancer Decision

This is the most commonly asked comparison for Indian and Filipino freelancers. Both platforms receive international income and send to local banks. Here is the honest comparison:

| Factor | Wise | Payoneer |

| Exchange rate | Mid-market rate + transparent fee (0.4–1.5%) | Own rate (typically 1.5–3.0% above mid-market, varies) |

| Marketplace integration | Not directly integrated with Upwork/Fiverr as payout method | Directly integrated with Upwork, Fiverr, Airbnb, and 1,000+ marketplaces as payout option |

| Receiving US bank details | YES — US routing + account number | YES — Payoneer US payment service |

| Sending to Indian bank (INR) | YES — good corridor, transparent fee | YES — available, rate less favorable than Wise |

| Sending to Philippine bank (PHP) | YES — direct to BDO, BPI, etc. | YES — also supports Philippine banks |

| Card | Wise Mastercard debit card | Payoneer Mastercard debit card |

| Account fee | Free | Free (was USD 29.95/year; check current policy) |

| Customer support | Chat only | Phone support available |

| Best for | Direct client income, international transfers, better rates | Marketplace payouts (Upwork, Fiverr), higher volume B2B |

Recommendation: If your income comes primarily from Upwork, Fiverr, or other marketplaces: keep Payoneer for marketplace payout, then transfer to Wise for better rates when sending to your home bank. For direct client invoicing and payment: Wise is the superior choice in almost every corridor.

Wise vs Revolut: Which Is Better for Digital Nomads?

| Factor | Wise | Revolut |

| Exchange rate fairness | Always mid-market; transparent fee | Mid-market during market hours; markup on weekends + exotic currencies |

| Monthly fee | Free (personal) | Free plan available; Premium (GBP 9.99) for more features |

| ATM withdrawals free | 2 free per month up to USD 100 each | GBP 200/month free (standard), GBP 400 (Premium) |

| Local bank details | US, UK, EU, AUS, CAD, SGD, NZD | US, UK, EU (varies by plan) |

| Customer support | Chat | Chat (phone on Metal plan) |

| Cryptocurrency | No | Yes (buy, sell, hold crypto) |

| Stock trading | No | Yes (Revolut Invest) |

| Available in India | YES | LIMITED (Revolut availability in India varies) |

| Available in Philippines | YES | LIMITED |

| Best for | International transfers, income reception, consistent pricing | Daily spending, premium features, crypto, if based in UK/EU |

For Indian and Filipino digital nomads specifically: Wise is the clear choice due to consistent availability and better India/Philippines banking integration. Revolut’s limited availability in both markets is a significant practical disadvantage.

Wise vs Traditional Bank SWIFT Transfer: The Real Cost

| Cost Component | Wise (USD 1,000 to INR) | Traditional Bank SWIFT |

| Sending fee | USD 7–9 (0.7–0.9%) | USD 15–40 sending fee |

| Exchange rate markup | 0% (mid-market) | 1.5–3% above mid-market = USD 15–30 hidden |

| Receiving fee (Indian bank) | INR 500–1,000 SWIFT incoming fee | INR 500–1,500 SWIFT incoming fee |

| Total cost estimate | USD 7–9 + receiving fee | USD 30–70+ total (hidden + visible) |

| Speed | 1–2 business days typically | 2–5 business days |

| Transparency | All fees shown before you confirm | Full cost often unclear until it arrives |

For a USD 1,000 transfer: Wise saves approximately USD 20 to 60 compared to traditional bank SWIFT, primarily because of the exchange rate markup banks charge without disclosure.

Wise Limitations: What It Cannot Do

- No THB account: Cannot hold or receive Thai baht. Thailand-based nomads need a local Thai bank account for daily spending.

- Not a full bank: No interest on balances (unless using Wise’s interest feature where available). No credit products, no loans, no mortgages.

- Transfer limits: Personal accounts have daily and monthly transfer limits that vary by country. High-volume transfers may require business accounts.

- No cash deposits: Cannot deposit physical cash into Wise. Top up by bank transfer or card only.

- Customer support is chat-only: No phone support for personal accounts. Resolution time varies.

- Coverage gaps: Not all countries are fully supported. Check wise.com/help/articles/2897238 for current country availability.

Is Wise Safe? Security and Regulation

| WISE SECURITY AND REGULATION FCA regulated: Wise is regulated by the UK’s Financial Conduct Authority (FCA) as an e-money institution. Wise Payments Limited is also regulated in the EU (Central Bank of Lithuania), US (FinCEN registered, state-level MTL licenses), Australia (ASIC), Singapore (MAS), and other major jurisdictions. Client fund protection: Wise holds customer funds separately from company funds (safeguarding). This is different from bank deposit insurance but provides a meaningful level of protection for user balances. Security features: Two-factor authentication (2FA), biometric login, real-time transaction notifications, card freeze/unfreeze instantly via app, dedicated fraud monitoring team. Track record: Wise has operated since 2011, has processed trillions of dollars in transfers, and has not had a major security incident affecting customer funds. Wise is not a bank and does not have FSCS protection (UK) or FDIC protection (US). For large balances, use a regulated bank for storage and Wise for active transactions. |

Frequently Asked Questions

Is Wise good for digital nomads?

Yes. Wise is one of the best international financial tools for digital nomads due to its mid-market exchange rate, transparent fee structure, local bank account details in major markets (US, UK, EU, Australia), and global debit card. For Indian and Filipino digital nomads specifically, Wise handles USD/EUR income receipt and INR/PHP conversion very well.

Does Wise work in Thailand?

Wise works in Thailand for sending money, but Wise does not support Thai baht (THB) as an account currency. You cannot hold THB in Wise. Thailand-based nomads use Wise to receive international income and convert to THB for transfer to their Bangkok Bank or KBank account. The Wise debit card works at Thai ATMs and merchants accepting Mastercard.

How much does Wise charge for USD to INR transfers?

Wise charges approximately 0.6% to 0.9% of the transfer amount for USD to INR transfers, plus the mid-market exchange rate (no markup on the rate itself). On USD 1,000: approximately USD 6 to 9 in fees. Your Indian bank may charge an incoming SWIFT fee (INR 500 to 1,500) on top. The total cost is significantly less than traditional bank SWIFT transfers.

Can Filipino digital nomads use Wise to send money to BDO or BPI?

Yes. Wise supports direct bank transfers to BDO, BPI, Metrobank, UnionBank, Landbank, PNB, and other major Philippine banks. The fee for USD to PHP transfers is typically 0.7% to 1.1%. Transfers typically arrive within 0 to 1 business day. GCash direct delivery availability varies; check Wise’s current Philippine options.

Is Wise better than Payoneer for Indian and Filipino freelancers?

For direct client income: Wise is generally better due to significantly lower effective fees (mid-market rate + 0.7-1.0% vs Payoneer’s 1.5-3% all-in). For marketplace income (Upwork, Fiverr): Payoneer has direct integration as a payout method which Wise lacks. Many freelancers use both: Payoneer for marketplace payout collection, Wise for transferring to home bank at better rates.

Final Verdict: Is Wise Right for Your Nomad Setup?

| Wise earns its status as the standard recommendation for digital nomad international banking. The combination of mid-market rate transfers, local bank account details in major markets, and a genuinely useful global debit card covers the most important financial infrastructure needs for location-independent professionals. For Indian digital nomads: Wise is excellent for receiving overseas income and sending to NRE/NRO accounts. The transparent INR corridor fees and 1 to 2 day settlement make it significantly better than traditional bank SWIFT for recurring overseas income repatriation. For Filipino digital nomads: Wise handles Philippine bank transfers well. Pair with Payoneer if your income comes from Upwork or Fiverr, and use Wise for the final INR/PHP transfer for better rates. For Thailand-based nomads: Wise plus Bangkok Bank is the complete setup. Wise handles international income and conversion; Bangkok Bank handles daily Thai spending. Open a Wise account free — there is no monthly fee, and your first few months of international transfers will immediately demonstrate the fee savings over your current method. Recommended account type: Personal for most freelancers. Business account if you invoice clients as a registered business entity. |