| Filipino nationals can open a Thai bank account in Thailand, but eligibility depends on visa type. Filipino nationals can open a Thai bank account in Thailand, but eligibility depends on visa type. For Thai bank account Filipino nationals, LTR Visa holders (with BOI endorsement letter), Non-Immigrant visa holders with work permit, and holders of other long-stay visas are eligible. Tourist visa and visa-exempt entry holders are typically rejected at most branches. Bangkok Bank and Kasikorn Bank (KBank) are the two most accessible banks for Filipino nationals. Required documents: Philippine passport (e-Passport preferred), valid Thai visa, proof of Thai address (rental contract), passport photo, and initial deposit (THB 500 to 1,000). GCash does not work directly for Thai QR payments. For receiving international income, Wise is significantly more cost-effective than SWIFT transfers into a Thai bank account. Sending money from a Thai bank to Philippine accounts (BDO, BPI, Metrobank) is possible via SWIFT but Wise is cheaper. |

| QUICK ANSWER: How can Filipino citizens open a bank account in Thailand? Filipino citizens can open a Thai bank account by following these steps: Confirm you have a qualifying visa (LTR Visa, Non-Immigrant B with work permit, or Non-Immigrant O)Prepare: Philippine e-Passport, valid Thai visa, rental contract, passport photo, THB 500–1,000 initial deposit Choose a foreigner-friendly branch of Bangkok Bank or KBank (expat areas, large shopping malls)Visit the branch, request a foreign national account opening, and present your documents Complete the application form with your name exactly as on your passport and Thai address Make the initial deposit and receive your account number and ATM card Tourist visa holders are typically rejected. If you are on a tourist visa, use Wise as your primary financial tool until you have a long-stay visa. |

| DISCLAIMER Thai bank requirements for foreign nationals, including Filipino passport holders, can change without notice and vary by branch. Always verify current requirements directly with the bank before visiting. This is not financial or legal advice. |

Introduction

If you have been living in Thailand with your GCash and a Philippine bank card, you have probably already felt the friction: foreign card fees at every ATM, no PromptPay QR payments, difficulty setting up auto-debit for rent or utilities, and the nagging sense that you are operating outside the Thai financial system rather than inside it.

Opening a Thai bank account solves most of that friction — but it requires more preparation than most guides suggest. The visa type in your passport is the primary factor. The branch you choose matters almost as much. And there are several Philippine-specific considerations — from BIR disclosure to GCash compatibility to remittance options — that generic banking guides for expats never cover.

This guide covers all of it, specifically for Filipino nationals in Thailand.

OFW vs. Digital Nomad: A Key Distinction for Filipino Banking in Thailand

| IMPORTANT CONTEXT FOR FILIPINOS Filipino remote workers and digital nomads in Thailand are NOT classified as Overseas Filipino Workers (OFWs) under the Philippines’ Department of Migrant Workers (DMW) framework. OFW status applies to Filipinos deployed abroad under POEA/DMW-processed employment contracts — typically factory workers, healthcare workers, seamen, or domestic workers. If you are a Filipino freelancer, remote software developer, BPO professional, or online business owner in Thailand, you are a Filipino citizen living abroad — not an OFW. This matters because: Thai banks treat you as a regular foreign national, not as a special OFW categoryOWWA benefits and DMW protections do not apply to your banking situation in ThailandYour Philippine banking obligations (BIR, SSS, PhilHealth) continue independently of your Thai bank account Many Filipino nomads in Thailand assume that OFW-specific Philippine banking products (BDO Kabayan, BPI Pamana) are relevant to their Thailand banking — they are not. Those products help you maintain Philippine accounts while abroad; they do not help you open a Thai account. |

Visa Requirements for Opening a Thai Bank Account as a Filipino

Your Philippine passport’s visa stamp is the primary factor in whether a Thai bank will open an account for you. Here is the current landscape:

| Visa Type | Account Opening Possibility | Notes for Filipinos |

| Thailand LTR Visa (WFT or other) | ✅ Easiest pathway | BOI endorsement letter is the strongest eligibility document. Most branches comfortable with LTR. |

| Non-Immigrant B (work visa) + Thai work permit | ✅ Standard pathway | Work permit required alongside the visa. Employer support helps. |

| Non-Immigrant O (retirement/family) | ✅ Possible | Supporting documents may be requested. Extension stamps showing long stay help. |

| SMART Visa holders | ✅ Possible | Recognized long-stay visa — accepted at most foreigner-capable branches. |

| Tourist Visa (TR) — 60 days | ⚠ Difficult | Most branches decline. Some tourist-area branches accept with strong supporting docs. Inconsistent. |

| 30-day visa-exempt entry stamp | ✖ Not recommended | Tourist profile — virtually all branches will decline. Use Wise as alternative. |

| MOST FILIPINOS IN THAILAND DON’T REALIZE THIS Filipino travelers frequently enter Thailand on visa-exempt 30-day stamps and then wonder why they cannot open a Thai bank account despite having all other documents ready. The 30-day visa-exempt stamp signals to Thai banks that you are a short-term tourist — not a long-stay resident. No amount of other documentation compensates for this. If you are planning to stay in Thailand long-term and need a Thai bank account, the LTR Visa is the most reliable path. The BOI endorsement letter functions as proof of legitimate long-stay status that Thai banks understand and accept. |

Which Thai Banks Accept Filipino Nationals?

Not all Thai banks are equally accessible for foreign nationals. The most reliable options for Filipino passport holders:

| Bank | Accessibility for Filipinos | Notes |

| Bangkok Bank (Kasikorn) | Good — most internationally experienced | Thailand’s largest bank. Foreigner-experienced branches in expat areas. SWIFT international transfer capability. |

| Kasikorn Bank (KBank) | Good — strong tech, foreigner familiar | Excellent mobile banking app. Very popular with digital nomads. QR payment system widely used. |

| SCB (Siam Commercial Bank) | Moderate — some branches accept foreigners | Less consistent than Bangkok Bank or KBank for foreign nationals. Try SCB branches in major malls. |

| Krungthai Bank (KTB) | Moderate | Government-linked bank. Some foreigner capability but less common for long-stay foreigners. |

| TMBThanachart (TTB) | Lower — less foreigner focus | Smaller international focus. Not the first choice for Filipino nationals. |

For most Filipino nationals in Thailand, the choice is between Bangkok Bank and KBank. Both are solid; KBank has a better mobile app; Bangkok Bank has a stronger international transfer network. Many Filipino nomads maintain accounts at both.

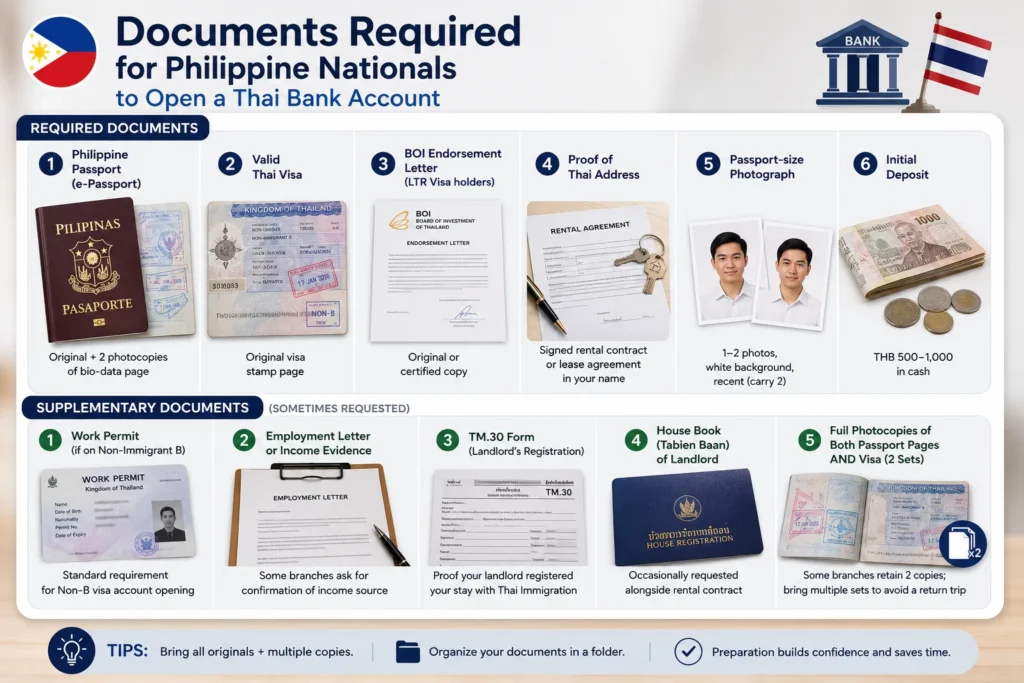

Documents Required for Philippine Nationals

| Document | Specification | Philippine-Specific Notes |

| Philippine passport (e-Passport) | Original + 2 photocopies of bio-data page | e-Passport (biometric, machine-readable) strongly preferred over older booklets. Some branches require it. |

| Valid Thai visa | Original visa stamp page | Must be non-tourist type for reliable results (see visa table above) |

| BOI endorsement letter (LTR Visa holders) | Original or certified copy | Strongest eligibility proof if on LTR Visa |

| Proof of Thai address | Signed rental contract or lease agreement in your name | Hotel booking not accepted. Private rental or serviced apartment with proper contract. |

| Passport-size photograph | 1–2 photos, white background, recent | Carry 2; not always required but avoids being sent away |

| Initial deposit | THB 500–1,000 in cash | Required on opening day. ATMs available near most branches. |

Supplementary documents (sometimes requested)

| Document | When requested |

| Work permit (if on Non-Immigrant B) | Standard requirement for Non-B visa account opening |

| Employment letter or income evidence | Some branches ask for confirmation of income source — useful to have |

| TM.30 form (landlord’s registration) | Proof your landlord registered your stay with Thai Immigration |

| House book (Tabien Baan) of landlord | Occasionally requested alongside rental contract |

| Full photocopies of both passport pages AND visa (2 sets) | Some branches retain 2 copies; bring multiple sets to avoid a return trip |

Step-by-Step: How to Open a Thai Bank Account as a Filipino

| STEP 1 | Confirm Your Visa Type and Choose Your Bank Verify that your Thai visa qualifies for account opening (LTR, Non-B with work permit, Non-O). Then choose between Bangkok Bank and KBank based on your priorities: Bangkok Bank for stronger international SWIFT capabilities; KBank for a better mobile app and more modern QR payment features. ⚡ Tip: Call the specific branch ahead of time and say: ‘I have a Philippine passport and an LTR Visa — can I open a savings account?’ This confirms the branch’s ability before you travel there. |

| STEP 2 | Prepare Your Documents (PH-Specific) Bring: Philippine e-Passport (original + 2 photocopies), valid Thai visa copy, BOI endorsement letter (if LTR), rental contract, 1–2 passport photos (white background), and THB 500–1,000 in cash. Also bring: your Philippine bank debit card (to have as backup) and your Wise card if you have one. ⚡ Tip: Bring your documents in a folder, organized in order: passport, visa, endorsement letter, rental contract, photos. Looking organized signals to staff that you are a prepared, credible customer. |

| STEP 3 | Choose the Right Branch and Arrive Early Visit a branch in an expat-heavy area: Sukhumvit, Silom, Sathorn (Bangkok), Nimman Road (Chiang Mai), or major shopping mall branches. Arrive between 9:30 and 11:30 AM on a weekday. Avoid arriving after 2:00 PM — staff are less receptive to complex foreign account applications late in the day. ⚡ Tip: Branches inside large shopping malls (Terminal 21, EmQuartier, CentralWorld, Siam Paragon) consistently have more experience with foreign nationals than neighborhood branches. |

| STEP 4 | Request the Customer Service Officer Ask at the reception or information desk for a customer service officer — not a teller — specifically about opening a new account as a foreign national. State your nationality and visa type clearly upfront. If the first officer seems uncertain, ask politely to speak with a senior officer or branch manager. ⚡ Tip: Use the phrase: ‘I have a Philippine passport and a Thailand LTR Visa. I would like to open a savings account.’ Being specific avoids confusion. |

| STEP 5 | Complete the Application Form Fill in all fields with your name exactly as printed on your passport, your Thai address from the rental contract, passport number, nationality (Filipino), and contact details. Double-check the spelling of your name before signing. Discrepancies between your account name and international transfer details cause delays. ⚡ Tip: If any field is unclear, ask the officer to clarify — do not guess. Incorrect information on the form may require the form to be resubmitted, which adds time. |

| STEP 6 | Deposit, Activate, and Set Up Mobile Banking Pay the THB 500–1,000 initial deposit. Receive your account number. Ask about the ATM card (issued same day at some branches; mailed in 3–5 days at others). Set up KBank’s app or Bangkok Bank’s Bualuang mBanking app at the branch with staff assistance. Confirm that your PromptPay mobile number registration is active. ⚡ Tip: Setting up PromptPay on your Thai number on the same day lets you receive local THB transfers immediately using your Thai phone number. |

GCash and Maya in Thailand: What Actually Works

This section answers the question that most Filipino nomads in Thailand have but cannot find a clear answer to online.

| GCASH AND MAYA IN THAILAND — HONEST ANSWER GCash: GCash does NOT work for Thai QR code payments (PromptPay or any Thai QR system)GCash International Remit allows you to send money from a Philippine GCash account to international recipients, but requires a linked Philippine bank accountIf someone in the Philippines sends money to you via GCash, you cannot receive it in Thailand directly to a Thai accountGCash can be used to pay some international merchants online (where Mastercard or Visa is accepted) via GCash Mastercard virtual card Maya (formerly PayMaya): Maya does NOT work for Thai local QR paymentsMaya Visa card can be used for online purchases where Visa is acceptedMaya accounts are Philippine-based and cannot substitute for a Thai bank account for local daily expenses Bottom line: For daily life in Thailand (rent, utilities, local transfers, PromptPay QR), you need a Thai bank account or a Wise card with THB functionality. |

Sending Money from Thailand to the Philippines

Once your Thai bank account is set up, you have two main options for sending money home to the Philippines:

Option 1: SWIFT transfer from Thai bank to Philippine bank

Bangkok Bank and KBank both support SWIFT transfers to Philippine banks. To send to a Philippine account (BDO, BPI, Metrobank, UnionBank, etc.):

- Your Philippine bank’s SWIFT code (e.g., BNORPHMM for BDO, BOPIPHM1 for BPI)

- Account holder name, account number, and bank branch

- Purpose of transfer (required field for Bank of Thailand compliance)

- Fees: typically THB 400–500 per outgoing SWIFT transfer + exchange rate spread of 1–2%

- Transfer time: 1 to 3 business days

Option 2: Wise (recommended for most amounts)

For regular or larger remittances to the Philippines, Wise is significantly cheaper than SWIFT transfers. Wise supports PHP as a receiving currency and integrates with Philippine bank accounts (BDO, BPI, UnionBank). The exchange rate is near mid-market with a flat fee of approximately 0.6 to 1.8% depending on the amount.

| Method | Fee Structure | Exchange Rate | Transfer Time | Best For |

| Bangkok Bank SWIFT | THB 400–500 + rate spread | Bank rate (1–2% below mid-market) | 1–3 business days | Infrequent large transfers |

| KBank SWIFT | Similar to Bangkok Bank | Similar bank rate | 1–3 business days | Same |

| Wise | 0.6–1.8% flat fee, near mid-market rate | Near mid-market (best available) | 1–2 business days | Regular remittances to PH |

| Western Union / Remitly | Fixed fee + margin | Below mid-market | Minutes to 1 day | Urgent small transfers |

BIR Awareness: Philippine Tax Implications of a Thai Bank Account

Filipino professionals in Thailand with a Thai bank account should be aware of their Philippine BIR (Bureau of Internal Revenue) obligations:

- Income earned and deposited into a Thai bank account is still subject to Philippine income tax if you remain a Philippine tax resident (spending more than 180 days in the Philippines per tax year)

- If you are spending more of the year outside the Philippines than in it, your tax residency status may change — consult a Philippine CPA or tax advisor

- Holding a foreign bank account does not automatically require BIR disclosure, but foreign-sourced income must be declared in your Philippine ITR (if you are still a Philippine tax resident)

- Philippine banks (BDO, BPI, Metrobank) are not automatically notified when you open a Thai account; however, regular large international wire transfers from a Thai account to a Philippine account may appear in your transaction records

| BIR DISCLAIMER BIR obligations for Filipinos earning and banking abroad are complex and depend on your specific residency status, income source, and the amount involved. Consult a Philippine CPA specializing in overseas Filipino tax compliance for guidance specific to your situation. This is not tax advice. |

SSS, PhilHealth, and Pag-IBIG Payments from Thailand

Opening a Thai bank account does not affect your Philippine social contribution obligations. Many Filipino nomads in Thailand continue their voluntary SSS, PhilHealth, and Pag-IBIG payments through:

- SSS online payment via My. SSS portal using a Philippine bank card or GCash (from a Philippine-linked GCash account)

- PhilHealth voluntary contributions via their online portal or partner payment channels

- Pag-IBIG Fund via their virtual Pag-IBIG (VPAL) online payment system

- Remittance services that handle Philippine government payment collection

Your Thai bank account is separate from these obligations. If you want to use your Thai account for Philippine government payment channels, this is generally not possible as those channels are Philippine-peso-denominated and require Philippine payment methods.

Bangkok Bank vs. KBank vs. Wise for Filipinos in Thailand

| Feature | Bangkok Bank | KBank | Wise |

| Account opening difficulty (for Filipinos) | Medium — visa dependent | Medium — similar to Bangkok Bank | Easy — online, no Thai visa needed |

| International SWIFT transfers | Full SWIFT support to Philippines | Full SWIFT support | Better rates than SWIFT; local PHP receiving |

| Mobile app quality | Good (Bualuang mBanking) | Excellent (KBank app) | Excellent (Wise app) |

| Thai QR (PromptPay) payments | Yes | Yes | Partial (Wise card for some QR) |

| Local Thai bill payments | Yes | Yes | Limited |

| PHP to THB conversion | Through SWIFT/FX desk | Through international transfer | Near mid-market rate |

| Sending money to PH (BDO, BPI) | SWIFT — THB 400–500 fee | SWIFT — similar fees | 0.6–1.8% flat fee, better rate |

| GCash/Maya integration | No | No | No direct integration |

| Best for | Local Thai expenses, formal banking | Best mobile experience | International income, PH remittances |

The Smart Setup: Wise + Thai Bank for Filipino Remote Workers

The most cost-effective banking setup for Filipino nomads in Thailand combines two tools for two different purposes:

| RECOMMENDED BANKING SETUP FOR FILIPINOS IN THAILAND Wise (for international income and Philippine remittances): Open Wise online using your Philippine passport and address — no Thai visa requiredGet a USD, EUR, GBP account to receive freelance income from Upwork, clients, or overseas employersConvert to PHP and send directly to BDO, BPI, or UnionBank in the Philippines at near mid-market ratesConvert to THB and send to your Thai bank account for local Thai expensesWise debit card accepted at international merchants and some Thai ATMs Thai Bank Account — Bangkok Bank or KBank (for local Thai life): Receive THB from Wise after converting international incomePay rent via bank transfer or PromptPay QRPay Thai utilities, internet, and subscriptionsLocal ATM withdrawals without foreign card feesRequired for many formal Thai financial activities Why this matters for Filipinos specifically: Wise lets you keep a PHP-receiving account for family remittances while using your Thai bank for day-to-day Thai life — avoiding the double-conversion cost of SWIFT. |

Common Mistakes Filipino Nationals Make

| Mistake | Consequence | Prevention |

| Attempting to open a Thai bank account on a tourist visa or visa-exempt stamp | Rejection at virtually all branches | Apply for LTR Visa first or use Wise until long-stay visa is in hand |

| Bringing an older non-biometric Philippine passport | Some branches specifically require e-Passport | Renew to e-Passport before applying; ensure it has at least 18 months remaining validity |

| Expecting GCash to work for Thai QR payments | GCash cannot process Thai PromptPay QR codes | Set up PromptPay on your Thai bank account and Thai SIM number for local QR payments |

| Not bringing rental contract (using hotel booking instead) | Hotel booking not accepted as proof of address | Secure a signed rental contract in your name before visiting the bank |

| Thinking all Thai branches are the same | Neighborhood branches reject foreign nationals; expat-area branches accept | Choose Sukhumvit, Silom, Sathorn, or major mall branches |

| Delaying account opening until you need money urgently | Account opening takes a morning; if rejected, you need time to try another bank | Open your Thai account in the first 1–2 weeks of your long-stay visa activation |

What to Do If Your Application Is Rejected

- Try a different branch in a more foreigner-experienced location. Same documents, different branch, often different result.

- Try the other main bank: if Bangkok Bank rejected you, try KBank (or vice versa).

- Use Wise as a complete interim banking solution. Wise handles international income, THB conversion, and Philippine remittances fully online without any Thai visa requirement.

- Improve your documentation: if rejection was due to visa type (tourist visa), work toward a long-stay visa before reapplying.

- Contact Bangkok Bank or KBank head office: for LTR Visa holders rejected at branch level, escalating to the bank’s international division can resolve the issue.

Frequently Asked Questions

How can Filipino citizens open a bank account in Thailand?

Filipino citizens can open a Thai savings account at Bangkok Bank or Kasikorn Bank (KBank) by presenting: a Philippine e-Passport, a valid long-stay Thai visa (LTR Visa, Non-Immigrant B with work permit, or Non-Immigrant O), a rental contract for their Thai address, a passport photo, and an initial deposit of THB 500 to 1,000. Tourist visa and visa-exempt entry holders are typically rejected. Choose branches in expat-heavy areas such as Sukhumvit, Silom, or major shopping malls.

Can I use GCash for payments in Thailand?

GCash cannot be used for Thai PromptPay QR code payments or for local Thai merchant transactions that require a Thai payment system. GCash Mastercard can be used for online purchases at merchants that accept international Mastercard. For day-to-day payments in Thailand (including QR), you need a Thai bank account with PromptPay registration or a Wise card.

How do I send money from Thailand to the Philippines?

Two main options: SWIFT transfer from Bangkok Bank or KBank to your Philippine bank account (BDO, BPI, Metrobank) at THB 400 to 500 per transfer plus exchange rate spread; or Wise, which sends at near mid-market rates with a flat fee of approximately 0.6 to 1.8%. For regular remittances to the Philippines, Wise is significantly cheaper.

Does having a Thai bank account affect my BIR obligations?

Having a Thai bank account does not automatically change your BIR obligations. However, foreign-sourced income deposited in a Thai account remains subject to Philippine income tax if you are still a Philippine tax resident. If you are spending most of the year in Thailand and qualify as a non-resident for Philippine tax purposes, your obligations change. Consult a Philippine CPA for your specific situation.

Is a Thai bank account necessary if I have Wise?

For many Filipino remote workers, Wise alone is sufficient for international income and Philippine remittances. However, a Thai bank account is necessary for: paying rent via local bank transfer or PromptPay, local Thai utility and bill payments, Thai QR code merchant payments, and any formal financial activity that requires a local Thai account. The recommended setup uses both Wise (for international income) and a Thai bank (for local Thai expenses).

Final Verdict

| For Filipino remote workers and digital nomads on long-stay visas in Thailand, a Thai bank account is a genuine quality-of-life improvement for daily local financial life. The process requires preparation — the right visa, the right documents, and the right branch — but it is not complicated once those elements are in place. Wise remains the better tool for international income and Philippine remittances. Bangkok Bank or KBank is better for local Thai financial life. Using both creates a complete, cost-effective system that handles everything from Upwork payments to Thai rent without unnecessary fees. If you are still on a tourist visa or visa-exempt entry, use Wise now and set up your Thai bank account once your LTR Visa or Non-Immigrant visa is issued. |