| British citizens are fully eligible for the Thailand LTR Visa (Long-Term Resident, Work-From-Thailand Professional category) with no nationality restriction. The income requirement is USD 40,000/year (approximately £32,000 at current rates) from non-Thai overseas sources. HMRC income documentation — Self Assessment Tax Return (SA100/SA302), P60, and UK bank statements — is accepted by BOI in place of the CA certificate required from Indian applicants. For Thailand LTR Visa British Citizens, a crucial advantage is that the UK uses a residence-based (not citizenship-based) tax system: British nationals who meet HMRC’s Statutory Residence Test conditions for non-residency are generally not liable for UK income tax on overseas earnings while living in Thailand. This is a significant advantage over American applicants, who pay US taxes on worldwide income regardless of residence. National Insurance contribution obligations and UK pension considerations continue to apply. |

| QUICK ANSWER: Can British citizens apply for Thailand LTR Visa? Yes. British citizens are fully eligible for the Thailand LTR Visa. Key facts: Income: USD 40,000/year (approx. £32,000) gross from non-Thai overseas sourcesExperience: 5+ years in your professional fieldHealth insurance: International plan with USD 50,000+ coverage valid in ThailandDocumentation: SA100 tax return (2 years), P60 or SA302, UK bank statements. No CA certificate required.UK tax advantage: British nationals who become non-UK tax resident are generally NOT taxed on overseas earnings — unlike US citizens who pay worldwide tax regardless of location UK nationals have one of the cleanest tax positions of any LTR Visa applicant nationality: leave the UK properly, establish non-residency under the Statutory Residence Test, and your overseas earnings are generally free of UK income tax. |

| DISCLAIMER This guide is for informational purposes only. UK tax residency, HMRC rules, BOI requirements, and Thai immigration policies can change. Always consult a UK tax specialist or qualified accountant for HMRC matters and a licensed Thai immigration consultant for LTR Visa guidance. This is not legal, financial, or tax advice. |

Introduction: British Citizens and the Thailand LTR Visa

British nationals have been among Thailand’s most consistent long-stay visitors for decades — drawn by the climate, cost of living, and the easy friendliness of Thai daily life. For many UK professionals, Thailand has been a distant aspiration rather than a realistic long-term plan, largely because the tourist visa route felt legally uncertain and practically unstable.

The Thailand LTR Visa changes that picture. Launched by the Thailand Board of Investment in 2022, the Work-From-Thailand (WFT) Professional category gives British remote workers what they have needed: a 10-year, multiple-entry stay with explicit work authorization for overseas employers, no visa runs, and full Thai banking access. For a UK software developer, consultant, or online business owner earning USD 40,000+ from overseas clients, the LTR Visa is the correct legal foundation for long-term Thailand residence.

What makes this guide different from the generic LTR Visa guides: the UK-specific tax picture, the HMRC documentation requirements, the Statutory Residence Test explained plainly, and the post-Brexit context that makes the LTR Visa more strategically relevant for British professionals than ever before.

LTR Visa in GBP: What USD 40,000 Means for UK Professionals

| INCOME THRESHOLD IN GBP CONTEXT USD 40,000/year at approximately £0.79/USD = approximately £31,600–32,000/year gross from overseas sources. Monthly equivalent: approximately £2,600–2,700/month gross from overseas clients or employers. UK professionals who typically qualify: Senior software engineers at US or EU tech companies on remote contracts (£60,000–150,000+)UK-based consultants serving international clients (£40,000–80,000+ overseas revenue)Freelance developers, designers, or marketers with overseas client portfoliosUK-registered limited company directors with overseas revenue exceeding the thresholdRemote employees of UK companies with globally-sourced contracts Note: Income must be from NON-THAI, overseas sources. UK client income qualifies. Thai client income does not. |

Eligibility Requirements for British Citizens

| Requirement | Standard | UK-Specific Notes |

| Annual income | USD 40,000 (approx. £32,000) gross from overseas non-Thai sources | Includes income from UK employer, UK clients, and other overseas clients. Not Thai-client income. |

| Professional experience | 5 years in relevant professional field | UK employment history fully accepted. LinkedIn, CV, and UK employer references standard. |

| Health insurance | USD 50,000+ international coverage valid in Thailand | UK NHS does not cover Thailand. AXA PPP International, Cigna Global, or Bupa Global required. |

| Income documentation | Varies by nationality | SA100 Self Assessment return (2 years), SA302 Tax Year Overview, P60 or P45, UK bank statements. No CA cert required. |

| Passport validity | Valid national passport | UK passport. Minimum 18 months remaining validity recommended. |

| Background check | BOI background review | Standard check. No UK-specific disqualifiers beyond criminal record issues. |

HMRC Income Documentation: What BOI Accepts from British Applicants

The BOI application requires evidence that you earn at least USD 40,000/year from overseas sources. For British nationals, HMRC-issued and HMRC-filed documents serve this purpose. No CA certificate is required.

For British employees (PAYE or remote employment)

| Document | UK Name | Specification |

| Tax return | SA100 (Self Assessment Tax Return) | Last 2 tax years. Available via HMRC personal tax account or accountant. |

| Tax year overview | SA302 (Tax Year Overview) | HMRC-generated confirmation of your tax position. Accepted by most lenders and institutions including BOI. |

| Employment income summary | P60 (End of Year Certificate) | From employer confirming gross salary and tax paid. Last 2 years. |

| Employment contract | Formal employment contract or offer letter | Confirming remote work arrangement, salary, and overseas employer details. |

| Bank statements | UK bank statements (Barclays, HSBC, Lloyds, NatWest, Santander) | 12 months showing salary or client payments. Highlight overseas income credits. |

For British freelancers and limited company directors

| Document | UK Equivalent | Specification |

| Tax return | SA100 + Schedule (Self Employment pages) | Last 2 tax years. Shows gross turnover from self-employment. |

| Accountant certification | Letter from ICAEW or ACCA-registered accountant | Confirming annual gross income from overseas sources. ICAEW/ACCA membership credentials included. UK equivalent of the CA certificate. |

| Company accounts | Limited company annual accounts (Companies House filed) | If operating via Ltd company. Shows turnover and retained profit. |

| Client contracts | Service agreements with overseas clients | 3 to 5 representative contracts showing client country, scope, and fees. |

| Bank statements | UK business or personal bank statements | 12 months. Business bank: Starling, Monzo Business, Barclays Business. Highlight overseas client payments. |

| WHAT BRITISH APPLICANTS DO NOT NEED British nationals do NOT need a CA certificate (the ICAI-issued document required from Indian applicants). HMRC Self Assessment documentation — SA100, SA302, and P60 — is the UK equivalent and is accepted by BOI. For self-employed British nationals: an accountant’s letter from an ICAEW or ACCA-registered accountant serves the same purpose as the Indian CA certificate. Make sure the letter explicitly confirms your gross income from overseas sources, your accountant’s professional body registration number, and their firm stamp and signature. |

Step-by-Step Application Process for British Citizens

- Confirm eligibility: Verify gross income from UK or overseas non-Thai sources exceeds USD 40,000 (approx. £32,000) for the most recent 12 months

- Gather HMRC documentation: Collect SA100 or SA302 (last 2 tax years), P60 or accountant’s letter, and 12 months of UK bank statements

- Obtain international health insurance: Purchase AXA PPP International, Cigna Global, or Bupa Global with USD 50,000+ Thailand coverage. NHS coverage does not qualify.

- Prepare your CV: Confirm 5+ years of professional experience documented with dates

- Assemble supporting documents: Employment contract or client agreements, professional certifications if applicable

- Register on BOI portal: Create an account at ltrvisat.boi.go.th

- Submit online application: Complete the form, upload all documents, pay the THB 50,000 (approx. £1,100) non-refundable endorsement fee

- Monitor BOI review: 20 to 35 working days. Check email for Additional Information Requests

- Receive BOI endorsement letter by email

- Book Thai Embassy appointment: Royal Thai Embassy London (Queen’s Gate, Kensington). Pay the THB 10,000 (£220) visa stamp fee

- Travel to Thailand and activate your LTR Visa on first entry

Cost Breakdown in GBP for British Applicants

| Cost Item | GBP (approx.) | Notes |

| BOI endorsement fee | £1,100 (THB 50,000) | Non-refundable. Paid online via BOI portal in THB. |

| Visa stamp fee (Thai Embassy London) | £220 (THB 10,000) | Paid at Royal Thai Embassy, Kensington, London. |

| International health insurance (annual) | £700–1,500/year | AXA PPP International, Cigna Global, or Bupa Global. |

| Accountant’s certification (if self-employed) | £150–400 | One-time ICAEW/ACCA accountant letter for income proof. |

| TOTAL first year (excluding insurance) | Approx. £1,320–1,500 | Insurance adds £700–1,500 annually. |

| Annual ongoing cost (health insurance only) | £700–1,500/year | Only ongoing visa-related expense for 10 years. |

UK Tax Implications: The Statutory Residence Test

This is the section that separates this guide from every other Thailand LTR Visa article aimed at British readers. The UK’s tax position for expats is fundamentally different from the US position — and significantly more advantageous.

How UK taxation works for British expats

Unlike the United States, the United Kingdom uses a residence-based tax system, not a citizenship-based one. This means:

- UK citizens who become non-UK tax residents are generally NOT liable for UK income tax on income earned outside the UK

- Once non-resident for UK tax purposes, overseas earnings — including income from overseas employers or clients earned while living in Thailand — are typically outside the scope of UK income tax

- UK-sourced income (rental income from UK property, UK dividends, UK pensions) typically remains taxable in the UK even for non-residents

The Statutory Residence Test (SRT)

HMRC’s Statutory Residence Test determines whether you are a UK tax resident in a given tax year (6 April to 5 April). The key tests for those planning to leave the UK for Thailand:

| SRT Component | Key Rule for UK-to-Thailand Movers |

| Automatic Overseas Test | If you spend fewer than 16 days in the UK in a tax year AND were UK-resident in previous years, you are automatically non-UK resident. Under 46 days if not UK-resident in any of the prior 3 tax years. |

| Automatic UK Test | If you spend 183+ days in the UK in a tax year, you are automatically UK-resident regardless of other factors. |

| Sufficient Ties Test | For those spending 16 to 182 days in the UK, HMRC applies a ties test (family, accommodation, work, 90-day, country ties). Fewer UK ties allow more days. |

| Split Year Treatment | In the year you leave the UK permanently, Split Year Treatment may apply — you are treated as non-resident from the date of departure, not the full tax year. |

| PRACTICAL IMPLICATION FOR UK-TO-THAILAND MOVES A British professional who moves to Thailand on an LTR Visa and spends fewer than 16 days in the UK per tax year will typically qualify as non-UK tax resident under the Automatic Overseas Test. As a non-UK tax resident, they are generally not liable for UK income tax on their overseas earnings (income from overseas clients or employers). Income from UK sources (UK rental income, UK savings interest, UK dividends) typically remains UK-taxable. This is a significant advantage over American LTR Visa holders, who pay US taxes on worldwide income regardless of residence. British nationals have a genuinely cleaner tax exit from their home country when living abroad. This is general information only. Your specific SRT outcome depends on your UK ties, days in UK, and income structure. Consult a UK tax specialist. |

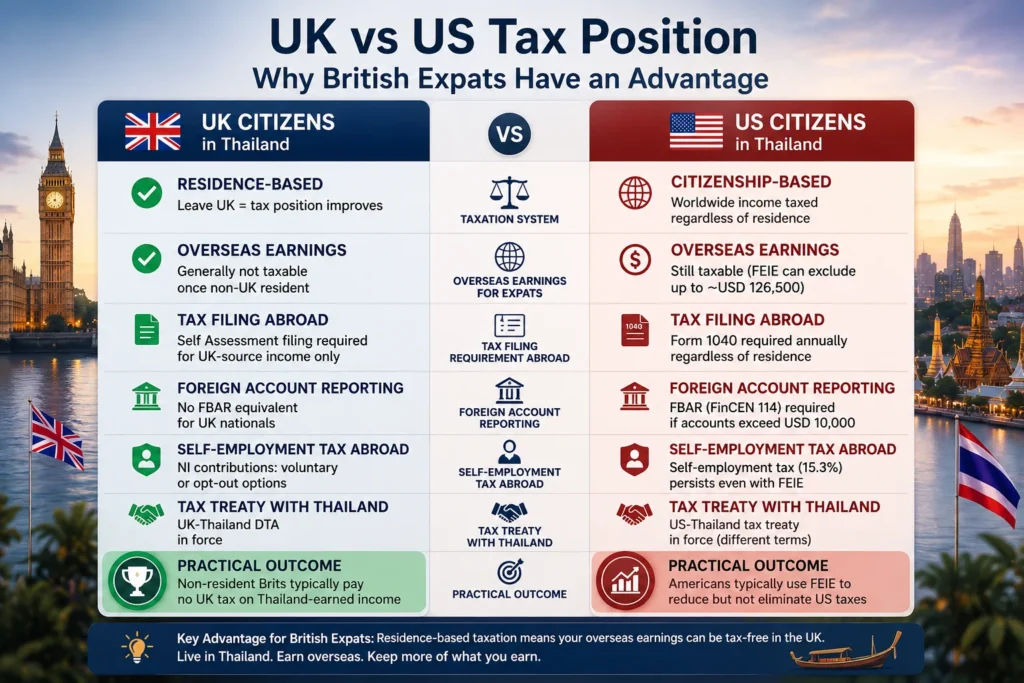

UK vs US Tax Position: Why British Expats Have an Advantage

| Tax Dimension | UK Citizens in Thailand | US Citizens in Thailand |

| Taxation system | Residence-based (leave UK = tax position improves) | Citizenship-based (worldwide income taxed regardless of residence) |

| Overseas earnings for expats | Generally not taxable once non-UK resident | Still taxable (FEIE can exclude up to ∼USD 126,500) |

| Tax filing requirement abroad | Self Assessment filing required for UK-source income only | Form 1040 required annually regardless of residence |

| Foreign account reporting | No FBAR equivalent for UK nationals | FBAR (FinCEN 114) required if foreign accounts exceed USD 10,000 |

| Self-employment tax abroad | NI contributions: voluntary or opt-out options | Self-employment tax (15.3%) persists even with FEIE |

| Tax treaty with Thailand | UK-Thailand DTA in force | US-Thailand tax treaty in force (different terms) |

| Practical outcome | Non-resident Brits typically pay no UK tax on Thailand-earned income | Americans typically use FEIE to reduce but not eliminate US taxes |

UK National Insurance Considerations for British Nationals in Thailand

National Insurance (NI) is separate from income tax and has its own rules for British nationals living abroad:

- If you leave the UK for Thailand and are no longer working for a UK employer, your NI contribution obligations typically end

- Self-employed UK nationals living abroad may be able to pay voluntary Class 2 or Class 3 NI contributions to maintain State Pension entitlement — at a relatively low cost (£3.45/week for Class 2 or £17.45/week for Class 3 in 2024/25)

- UK State Pension entitlement requires 35 qualifying NI years for the full new State Pension. Voluntary contributions from Thailand can protect this entitlement during long-term overseas residence

- UK company employees sent abroad may have NI liability under the company’s employer obligations, separate from personal NI

| STATE PENSION PLANNING NOTE British nationals planning to live in Thailand for 5+ years should review their National Insurance record before departing the UK. Check your NI contribution history via the HMRC personal tax account (gov.uk) to identify any gaps. Consider whether voluntary contributions are worth making to protect full State Pension entitlement. The cost of voluntary Class 2 contributions while abroad is low relative to the long-term State Pension benefit. This is not financial advice — consult a UK financial planner. |

UK-Thailand Double Taxation Agreement

The UK and Thailand have a Double Taxation Agreement (DTA) in force, covering income tax and specific types of income. Key points for British LTR Visa holders:

- The DTA establishes which country has primary taxing rights on different types of income (employment income, business profits, pensions, dividends, interest, royalties)

- For British nationals who become non-UK tax residents and earn income overseas: the DTA provides a framework for resolving any dual tax claims that might arise

- UK pension income paid to non-UK residents: the DTA may determine whether HMRC withholds UK tax at source or whether the income is taxable only in Thailand

- UK rental income for British nationals in Thailand: typically remains UK-taxable under both UK domestic law and the DTA, regardless of your residence status

| DTA DISCLAIMER The UK-Thailand DTA is a complex legal document. Its application depends on your specific income types, residency status in both countries, and the particular article of the DTA that applies. This overview is for general awareness only. Consult a UK tax specialist with international experience for your specific situation. |

Post-Brexit Context: Why the LTR Visa Matters More for British Nationals

Before Brexit, British citizens had EU freedom of movement — the right to live and work in any EU country indefinitely without a visa. That right ended on 31 December 2020. British nationals now face visa requirements to live long-term in EU countries that they did not face before.

This context matters for the Thailand LTR Visa in two ways:

- Thailand’s LTR Visa is accessible to British nationals on the same terms as before Brexit — EU membership never affected UK-Thailand bilateral visa arrangements. The LTR Visa represents a stable, long-term legal pathway for UK professionals who want an Asian base

- The LTR Visa’s 10-year duration compares favourably with the post-Brexit realities of long-term residence in EU countries, which now require national residency permit applications, integration requirements, and annual renewals in many cases

For British remote workers considering international bases, Thailand’s LTR Visa offers what post-Brexit EU residence no longer does automatically: stability, simplicity, and a decade of legal certainty.

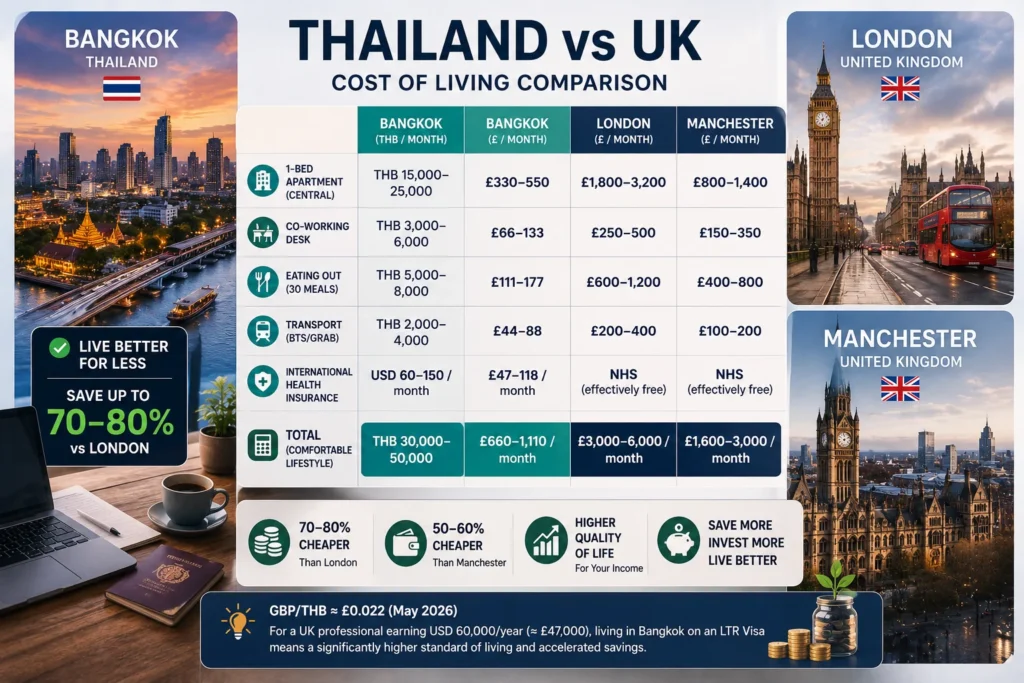

Thailand vs UK Cost of Living: The Financial Case

| Expense | Bangkok (THB/month) | Bangkok (£/month) | London (£/month) | Manchester (£/month) |

| 1-bed apartment (central) | THB 15,000–25,000 | £330–550 | £1,800–3,200 | £800–1,400 |

| Co-working desk | THB 3,000–6,000 | £66–133 | £250–500 | £150–350 |

| Eating out (30 meals) | THB 5,000–8,000 | £111–177 | £600–1,200 | £400–800 |

| Transport (BTS/Grab) | THB 2,000–4,000 | £44–88 | £200–400 | £100–200 |

| International health insurance | USD 60–150/month | £47–118/month | NHS (effectively free) | NHS (effectively free) |

| TOTAL (comfortable lifestyle) | THB 30,000–50,000 | £660–1,110/month | £3,000–6,000/month | £1,600–3,000/month |

Note: GBP/THB conversion at approximately £0.022 per THB (May 2026). The cost saving of Bangkok vs. London is approximately 70 to 80% for a comparable professional lifestyle. Even against Manchester, Bangkok is 50 to 60% cheaper. For a UK professional earning USD 60,000/year (approx. £47,000), living in Bangkok on an LTR Visa can convert into a significantly higher standard of living or accelerated savings than living in any UK city.

Common Mistakes British Applicants Make

| Mistake | Why It Matters | Prevention |

| Using a tax-reduced SA302 figure for the USD 40,000 threshold | If you’ve claimed business expenses, your SA302 shows taxable profit, not gross turnover. BOI wants gross income. | Submit gross turnover from SA100 plus an accountant letter confirming gross overseas income |

| Submitting NHS coverage as qualifying health insurance | NHS does not cover Thailand. BOI requires USD 50,000+ international coverage valid in Thailand. | Purchase AXA PPP International, Cigna Global, or Bupa Global before applying |

| Not consulting HMRC before cutting UK ties rapidly | Failing the Statutory Residence Test inadvertently or triggering HMRC scrutiny on departure timing | Consult a UK tax specialist about SRT implications before deciding how many days to spend in the UK |

| Assuming EU visa-free entry to Thailand still applies post-Brexit | It never applied through the EU. Thailand-UK bilateral terms were always separate. UK passport still gets 30-day visa-exempt access to Thailand. | UK passport gets 30 days visa-exempt entry to Thailand unchanged by Brexit |

| Applying without international health insurance in place | BOI requires proof of USD 50,000+ coverage at time of application. Cannot apply without it. | Purchase qualifying insurance before starting the BOI portal application |

Risks and Limitations for British Citizens on LTR Visa

- Health insurance ongoing cost: The NHS stops covering you for routine care once you are a non-UK tax resident living in Thailand long-term. International health insurance (£700 to 1,500/year) replaces this. For those with ongoing health needs, insurance underwriting and pre-existing condition exclusions are a genuine risk.

- UK rental income remains taxable: British nationals who keep UK property and earn UK rental income continue to be taxed in the UK on that income, regardless of non-resident status. Non-resident landlords must register with HMRC’s Non-Resident Landlord Scheme.

- 90-day address reporting in Thailand: LTR Visa holders must report their Thai address to Thai Immigration every 90 days. This is administrative rather than burdensome but requires awareness.

- Statutory Residence Test complexity: The SRT involves multiple tests and can produce unexpected results if you spend more UK days than planned. A failed SRT year means UK tax residency for that year.

- BOI fee is non-refundable: The THB 50,000 (£1,100) endorsement fee is lost if rejected. Prepare a complete application before submitting.

Frequently Asked Questions

Can British citizens apply for the Thailand LTR Visa?

Yes. UK citizens are fully eligible for the Thailand LTR Visa Work-From-Thailand Professional category. The income requirement is USD 40,000/year (approximately £32,000) from non-Thai overseas sources. UK nationals submit HMRC documentation — SA100 Self Assessment return, SA302, P60, and UK bank statements — in place of a CA certificate. The application process is the same as for all nationalities via the BOI portal.

What HMRC documents does BOI accept for the Thailand LTR Visa?

BOI accepts: SA100 Self Assessment Tax Return (2 years), SA302 Tax Year Overview, P60 (employees) or accountant’s letter from an ICAEW/ACCA-registered accountant (self-employed), employment contract or client agreements confirming overseas income, and 12 months of UK bank statements showing income credits. No CA certificate is required from British applicants.

Do British citizens still pay UK taxes when living in Thailand on LTR Visa?

It depends on your UK tax residency status. British nationals who meet HMRC’s Statutory Residence Test conditions for non-residency — typically by spending fewer than 16 days per year in the UK — are generally not liable for UK income tax on overseas earnings. UK-sourced income (UK rental income, UK dividends) typically remains UK-taxable even for non-residents. This is significantly more advantageous than the US position, where Americans pay worldwide tax regardless of residence.

Does moving to Thailand affect my UK State Pension?

Moving to Thailand does not cancel your existing UK State Pension entitlement. However, National Insurance contributions typically stop once you are no longer working in the UK. If you have fewer than 35 qualifying NI years, consider making voluntary Class 2 or Class 3 contributions to maintain or build State Pension entitlement. Check your NI record via HMRC’s government gateway before departing.

Where do British nationals apply for the Thailand LTR Visa stamp?

After receiving your BOI endorsement letter, book an appointment at the Royal Thai Embassy in London (29-30 Queen’s Gate, South Kensington, London SW7 5JB). The Thai Embassy London handles LTR Visa stamping for UK applicants. Pay the THB 10,000 (£220) visa fee at the appointment.

Final Verdict: Thailand LTR Visa for British Citizens

| British nationals are among the best-positioned LTR Visa applicants globally — not just because of the straightforward HMRC documentation, but because of the UK’s residence-based tax system. A British professional who establishes non-UK tax residency under the Statutory Residence Test and lives in Thailand can generally have their overseas earnings free of UK income tax, while an equivalent American pays US taxes on worldwide income regardless. The LTR Visa provides what post-Brexit Britain increasingly cannot: a stable, decade-long legal residence in a cost-effective, internationally connected, well-serviced country. The 10-year duration and no-visa-run structure are genuinely practical improvements over the tourist visa pattern that most UK professionals in Thailand have been using. The HMRC documentation process is manageable for any UK professional with a clean Self Assessment filing history. The health insurance cost replaces NHS coverage. The National Insurance voluntary contribution decision is worth reviewing before departure. Check the Thailand LTR Visa Complete Guide for the full application process, or compare Thailand vs other long-stay options in the Thailand Digital Nomad Visa Guide. |